Space Semiconductor Market

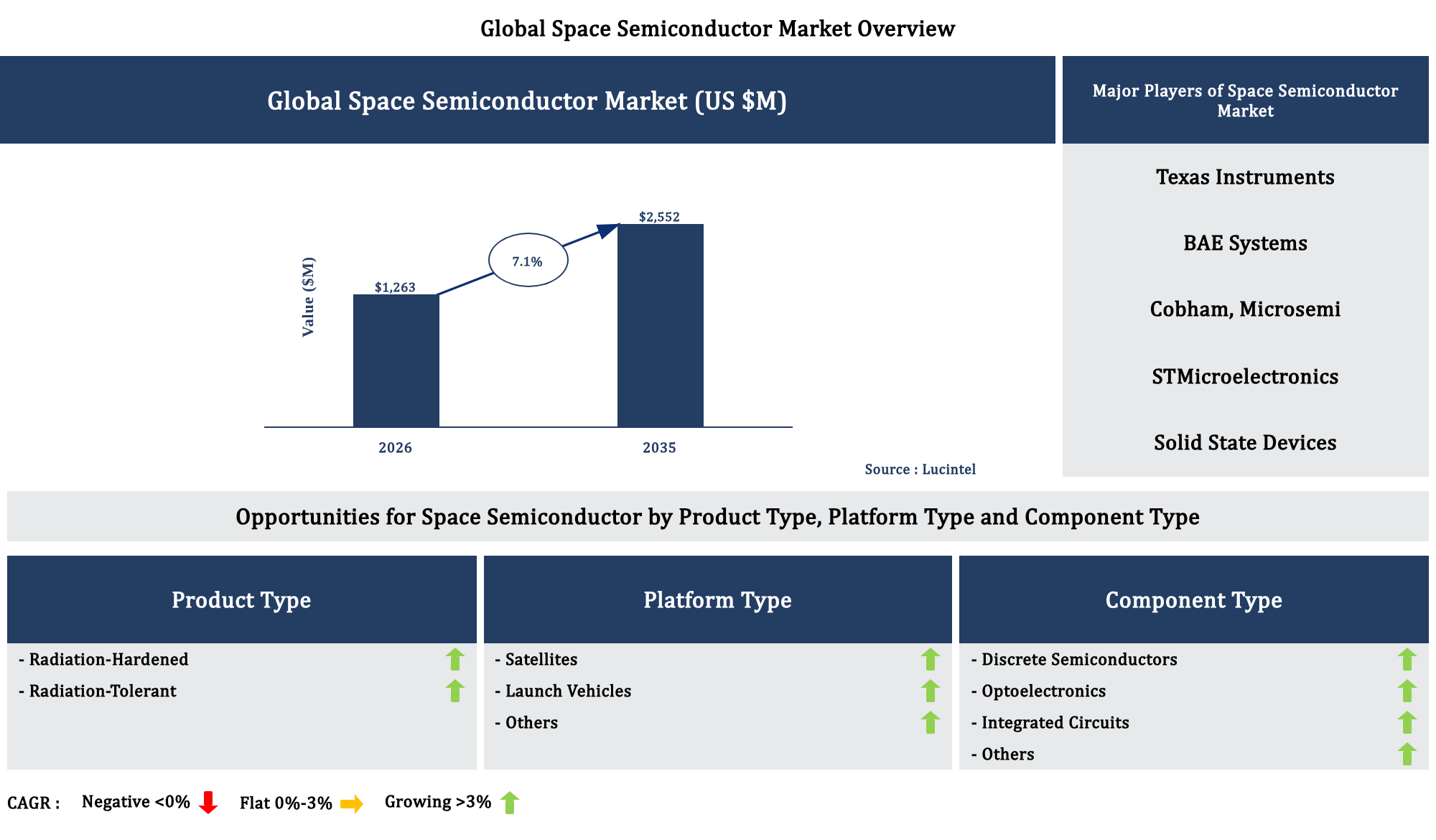

The future of the global space semiconductor market looks promising with opportunities in the discrete semiconductor, optoelectronic, and integrated circuit markets. The global space semiconductor market is expected to reach an estimated $2,552 million by 2035 with a CAGR of 7.1% from 2026 to 2035. The major drivers for this market are the rising demand for reliable & radiation hardened chips, the increasing demand for deep space missions & research activities, and the growing demand for private sector participation in space industry.

Gain valuable insights for your business decisions with our comprehensive 150+ page report. Sample figures with some insights are shown below.

Emerging Trends in the Space Semiconductor Market

The space semiconductor market is evolving rapidly as space missions become more complex, frequent, and commercially driven. Increasing deployment of satellite constellations, deep space exploration programs, and defense-focused space systems is accelerating demand for highly reliable and radiation-resistant semiconductor components. At the same time, advancements in materials science, miniaturization, and AI-enabled space electronics are reshaping how chips are designed and deployed. Governments and private companies are investing heavily in resilient supply chains and next-generation fabrication technologies. These developments are creating a highly competitive and innovation-driven market landscape, where performance, durability, and energy efficiency are becoming critical requirements for space-grade semiconductors.

These emerging trends are reshaping the space semiconductor market by driving innovation, improving reliability, and expanding commercial opportunities. Advances in radiation-resistant materials, AI-enabled computing, and miniaturization are enhancing mission capabilities, while growing satellite constellations are increasing demand at scale. At the same time, supply chain localization is strengthening national security and technological independence. Together, these trends are creating a more competitive, resilient, and technologically advanced global space semiconductor ecosystem.

Recent Developments in the Space Semiconductor Market

The space semiconductor market is witnessing rapid transformation driven by increasing satellite deployments, deep space missions, and rising demand for radiation-resistant and high-performance electronic components. Governments and private aerospace companies are heavily investing in advanced semiconductor technologies to support next-generation space applications. Developments in materials science, AI integration, and miniaturization are further accelerating innovation. At the same time, global competition is intensifying as countries focus on building secure, localized semiconductor supply chains to ensure strategic independence and technological leadership in space exploration and defense systems.

These developments are collectively transforming the space semiconductor market by enhancing performance, reliability, and scalability of space-grade electronic systems. The expansion of radiation-hardened manufacturing, AI-enabled computing, and advanced materials is enabling more complex and autonomous space missions. Meanwhile, growth in satellite constellations is increasing demand, and strategic supply chain investments are strengthening global resilience. Together, these changes are driving a more innovative, competitive, and technologically advanced market ecosystem that supports both commercial expansion and national security objectives in the global space industry.

Strategic Growth Opportunities in the Space Semiconductor Market

The space semiconductor market is experiencing expansion as applications continue to diversify across communication, defense, navigation, and scientific exploration. Increasing satellite deployments, deep space missions, and commercialization of space activities are driving demand for reliable, radiation-resistant, and energy-efficient semiconductor technologies. Governments and private companies are investing in advanced chip design and manufacturing capabilities to support next-generation missions. This environment is creating significant strategic growth opportunities across multiple applications, enabling innovation, improved performance, and long-term scalability in global space infrastructure ecosystems.

The growth opportunities are transforming the space semiconductor market by accelerating innovation and expanding application areas across communication, defense, exploration, and satellite systems. Rising investments in chip design, radiation-hardened technologies, and AI-enabled computing are improving performance and reliability of space electronics. At the same time, increasing commercialization of space activities is driving demand for cost-efficient semiconductor solutions. Strengthened supply chains and domestic manufacturing initiatives are enhancing resilience. Overall, these developments are reshaping competitive dynamics and enabling market growth across space ecosystems.

Space Semiconductor Market Drivers and Challenges

The space semiconductor market is influenced by a combination of technological advancements, economic investments, and regulatory frameworks that shape its growth trajectory. Increasing satellite deployments, defense requirements, and deep space missions are accelerating demand for reliable and high-performance semiconductor components. At the same time, factors such as supply chain constraints, high development costs, and strict compliance standards present notable challenges. Governments and private companies are actively investing in innovation and domestic manufacturing capabilities to address these issues. Overall, the interplay of these drivers and challenges is defining the pace and direction of market expansion globally.

The factors responsible for driving the space semiconductor market include:-

The challenges in the space semiconductor market are:

The space semiconductor market is shaped by strong growth drivers such as increasing satellite deployments, technological advancements, and rising investments in defense and commercial space activities. At the same time, challenges including high development costs, supply chain vulnerabilities, and stringent regulatory requirements create barriers to growth. The balance between innovation and cost efficiency remains critical for market participants. As governments and companies continue to invest in domestic capabilities and advanced technologies, the market is expected to evolve toward greater resilience, improved performance, and expanded commercial opportunities across global space ecosystems.

List of Space Semiconductor Market Companies

Companies in the market compete on the basis of product quality offered. Major players in this market focus on expanding their manufacturing facilities, R&D investments, infrastructural development, and leverage integration opportunities across the value chain. Through these strategies space semiconductor market companies cater increasing demand, ensure competitive effectiveness, develop innovative products & technologies, reduce production costs, and expand their customer base. Some of the space semiconductor market companies profiled in this report include-

Space Semiconductor Market by Segment

The study includes a forecast for the global space semiconductor market by product type, platform type, component type, and region.

Country Wise Outlook for the Space Semiconductor Market

The space semiconductor market is undergoing rapid transformation driven by rising satellite deployments, deep-space exploration programs, defense modernization, and the increasing demand for radiation-hardened and high-reliability chips. Governments and private firms are investing heavily in advanced fabrication capabilities, AI-enabled space systems, and resilient supply chains to support next-generation missions. Across major economies, recent developments reflect a shift toward self-reliance, strategic partnerships, and commercialization of space technologies. Countries such as the United States, China, Germany, India, and Japan are strengthening their semiconductor ecosystems through policy support, manufacturing expansion, and innovation in materials and chip design for harsh space environments.

Features of the Space Semiconductor Market

Top 5 Companies

Table of Contents

List of Figures

List of Tables

Methodology

Lucintel has been in the business of market research and management consulting since 2000 and has published over 1000 market intelligence reports in various markets / applications and served over 1,000 clients worldwide. This study is a culmination of four months of full-time effort performed by Lucintel's analyst team. The analysts used the following sources for the creation and completion of this valuable report:

- In-depth interviews of the major players in this market

- Detailed secondary research from competitors' financial statements and published data

- Extensive searches of published works, market, and database information pertaining to industry news, company press releases, and customer intentions

- A compilation of the experiences, judgments, and insights of Lucintel's professionals, who have analyzed and tracked this market over the years.

Extensive research and interviews are conducted across the supply chain of this market to estimate market share, market size, trends, drivers, challenges, and forecasts. Below is a brief summary of the primary interviews that were conducted by job function for this report.

Thus, Lucintel compiles vast amounts of data from numerous sources, validates the integrity of that data, and performs a comprehensive analysis. Lucintel then organizes the data, its findings, and insights into a concise report designed to support the strategic decision-making process. The figure below is a graphical representation of Lucintel's research process.

Buy Now

Choose a license that fits your team. Instant PDF delivery.

Prices exclude taxes. Instant delivery. Custom licensing available on request.

Frequently Asked Questions

What is the space semiconductor market size?

What is the growth forecast for space semiconductor market?

What are the major drivers influencing the growth of the space semiconductor market?

What are the major segments for space semiconductor market?

Who are the key space semiconductor market companies?

Some of the key space semiconductor companies are as follows:

- Texas Instruments

- BAE Systems

- Cobham, Microsemi

- STMicroelectronics

- Solid State Devices

Which space semiconductor market segment will be the largest in future?

In space semiconductor market, which region is expected to be the largest in next 8 years?

Do we receive customization in this report?

Key Questions

- • What are some of the most promising, high-growth opportunities for the space semiconductor market by product type (radiation-hardened and radiation-tolerant), platform type (satellites, launch vehicles, and others), component type (discrete semiconductors, optoelectronics, integrated circuits, and others), and region (North America, Europe, Asia Pacific, and the Rest of the World)?

- • Which segments will grow at a faster pace and why?

- • Which region will grow at a faster pace and why?

- • What are the key factors affecting market dynamics? What are the key challenges and business risks in this market?

- • What are the business risks and competitive threats in this market?

- • What are the emerging trends in this market and the reasons behind them?

- • What are some of the changing demands of customers in the market?

- • What are the new developments in the market? Which companies are leading these developments?

- • Who are the major players in this market? What strategic initiatives are key players pursuing for business growth?

- • What are some of the competing products in this market and how big of a threat do they pose for loss of market share by material or product substitution?

- • What M&A activity has occurred in the last 5 years and what has its impact been on the industry?