Polyimide Film Market

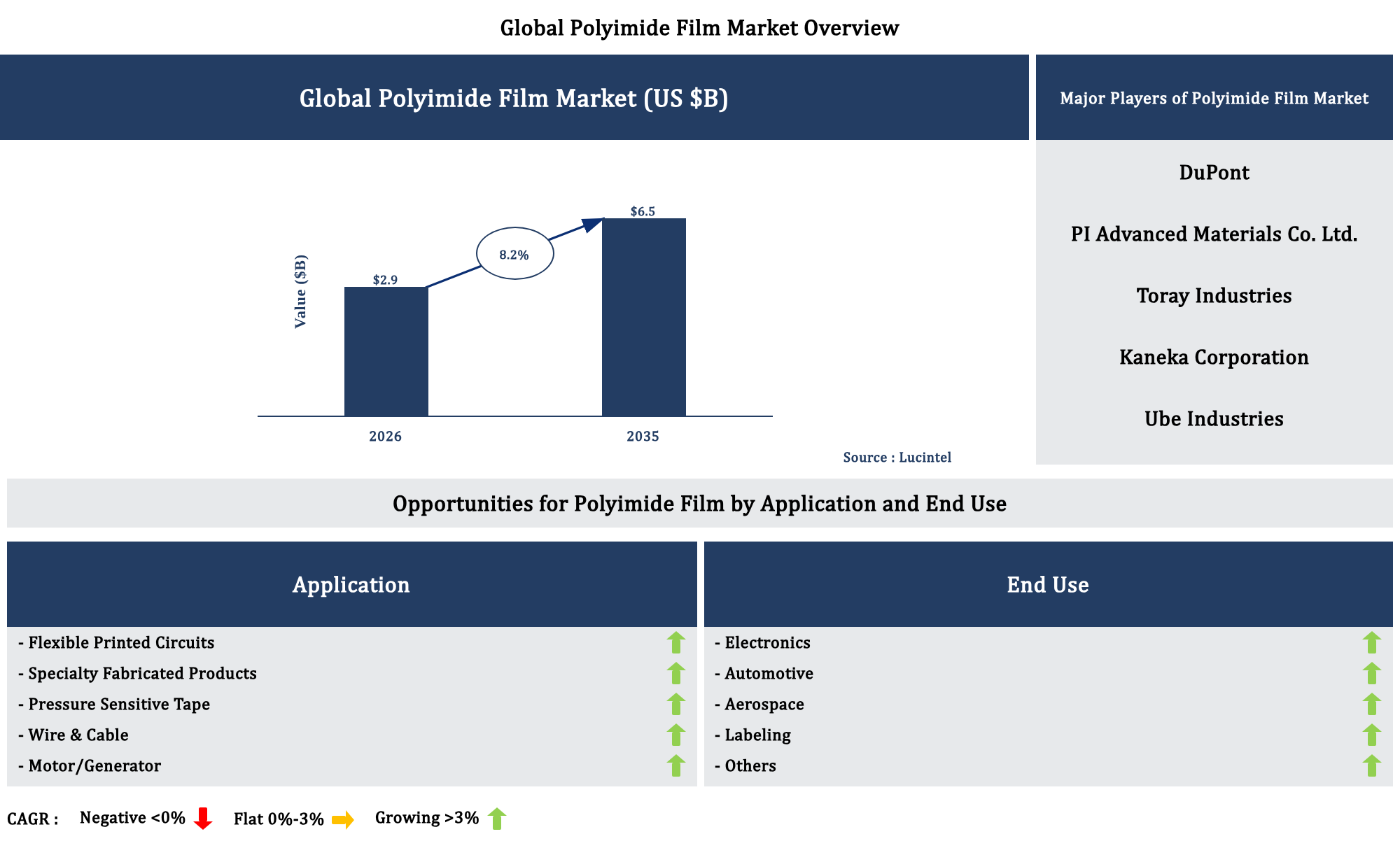

The future of the global polyimide film market looks promising with opportunities in the electronic, automotive, aerospace, and labeling markets. The global polyimide film market is expected to reach an estimated $6.5 billion by 2035 with a CAGR of 8.2% from 2026 to 2035. The major drivers for this market are the growing demand from automotive electronics & electric vehicles, the rising adoption in aerospace & defense applications, and the increasing demand for lightweight & durable materials.

Gain valuable insights for your business decisions with our comprehensive 150+ page report. Sample figures with some insights are shown below.

Emerging Trends in the Polyimide Film Market

The polyimide film market is evolving as demand rises across high temperature electronics, flexible devices, aerospace systems, and advanced industrial insulation. Manufacturers are responding with material innovations, process improvements, and partnerships to meet stricter performance requirements and faster qualification cycles. At the same time, sustainability expectations, volatile raw material costs, and supply chain disruptions are shaping procurement strategies. Key buyers are shifting from single-spec grades toward tailored films optimized for thermal stability, dielectric performance, mechanical strength, and manufacturability. These changes are driving investments in capacity expansion, thinner and defect-controlled products, and new formulations that improve yield. The market is also seeing stronger regulatory and customer scrutiny on lifecycle impacts.

These trends are reshaping the polyimide film market by moving it toward higher-performance, thinner, and more reliable grades, while accelerating innovations in adhesion, thermal durability, and manufacturability. Sustainability and regulatory pressure are influencing formulations and processing, and customers increasingly expect documented lifecycle and compliance support. Meanwhile, regional capacity expansion and stronger supply chain strategies are improving availability and shortening qualification cycles. Together, these forces are shifting competition from pure material cost toward total performance, yield impact, compliance readiness, and consistent supply, which will define purchasing decisions over the next several years.

Recent Developments in the Polyimide Film Market

The Polyimide films Market are increasingly used where heat, chemical resistance, and electrical insulation must survive harsh conditions. Over the last few years, demand has accelerated from consumer electronics to aerospace applications, driven by lighter, thinner designs and higher power densities. At the same time, manufacturers have improved coating, surface treatment, and thickness control to reduce defects. Policy pressure for lower emissions and end‑of‑life options is reshaping supply chains. The following developments highlight five growth opportunities in the polyimide film market today.

These five developments are expanding the polyimide film value chain beyond specialty grades into high-volume, performance-critical segments. Thinner, cleaner films for advanced interconnects and demanding automotive duty cycles are driving qualification wins. Aerospace innovations add lifecycle contracts, while medical-focused coatings support faster commercialization of wearable and disposable sensing. Sustainability and recycling initiatives further reduce costs and strengthen regulatory positioning. Together, they increase capacity utilization, encourage supply-chain consolidation, and raise long-term pricing power as customers prioritize reliability, compliance, and efficiency.

Strategic Growth Opportunities in the Polyimide Film Market

The polyimide film market demand is rising as electronics shrink, thermal requirements intensify, and manufacturers seek durable flexible materials. Growth is driven by flexible printed circuits, advanced insulation, and high-temperature coatings in automotive, aerospace, medical, and renewable energy systems. At the same time, improvements in film clarity, mechanical strength, and processability reduce integration barriers for OEMs and contract manufacturers. Strategic expansion across leading applications, supported by capacity scaling and compliance with reliability standards, can capture faster adoption cycles and higher-margin specialty grades.

Across flexible PCBs, telecom insulation, automotive battery and wiring, medical wearables, and aerospace/renewables, polyimide film can expand both volume and specialty mix. Each application values heat tolerance, electrical or mechanical reliability, and manufacturability, so investment in tailored grades, qualification testing, and regional capacity yields repeatable customer transitions. As supply chains mature, customers will favor suppliers that provide consistent thickness control, low outgassing, and documented traceability. Collectively these moves strengthen pricing power, reduce development lead times, and accelerate adoption of materials.

Polyimide Film Market Drivers and Challenges

The polyimide film market is shaped by technological, economic, and regulatory factors that influence both demand and production. Technological drivers such as advances in flexible electronics, improved thermal stability, and better film processing methods raise adoption in aerospace, automotive, and consumer devices. Economic forces including rising investment in semiconductors, overall manufacturing growth, and currency or raw material price volatility affect purchasing decisions and margins. Regulatory requirements related to emissions, workplace safety, and material compliance also steer product design and qualification timelines. Together, these factors determine market growth rates, regional competitiveness, and the pace at which new grades of polyimide films replace older insulation and packaging materials.

The factors responsible for driving the polyimide film market include:

The challenges facing this Market include:

The polyimide film market is driven by accelerating flexible electronics, expanded semiconductor manufacturing, and growing needs for high temperature insulation in industrial and aerospace applications. Continuous technical improvements in film properties and more efficient manufacturing strengthen competitiveness and broaden application potential. Meanwhile, investment in electrification and advanced manufacturing sustains long term demand. However, raw material price volatility, complex supply chains, and stringent customer qualification cycles can slow growth and adoption. Environmental and regulatory compliance requirements further raise costs and may force process changes. Overall, the market benefits from strong end demand, but performance consistency, risk management, and compliance readiness determine who captures sustainable share.

List of Polyimide Film Market Companies

Companies in the market compete on the basis of product quality offered. Major players in this market focus on expanding their manufacturing facilities, R&D investments, infrastructural development, and leverage integration opportunities across the value chain. Through these strategies polyimide film market companies cater increasing demand, ensure competitive effectiveness, develop innovative products & technologies, reduce production costs, and expand their customer base. Some of the polyimide film market companies profiled in this report include-

Polyimide Film Market by Segment

The study includes a forecast for the global polyimide film market by application, end use, and region.

Country Wise Outlook for the Polyimide Film Market

The polyimide film market is being reshaped by rapid growth in flexible and high-reliability electronics, alongside rising demand for thermal insulation, dielectric performance, and lightweight materials in electric vehicles and industrial equipment. Over the last few years, customers have tightened requirements for heat resistance, dimensional stability, low outgassing, and processability in advanced manufacturing. At the same time, supply chains have expanded and diversified, with new capacity coming online, more investment in specialty grades, and stronger emphasis on quality certification. Across the United States, China, Germany, India, and Japan, these shifts are reflected in project announcements, qualification of new materials, and partnerships that target next-generation semiconductor packaging and flexible display applications.

Features of the Polyimide Film Market

Top 5 Companies

Table of Contents

List of Figures

List of Tables

Methodology

Lucintel has been in the business of market research and management consulting since 2000 and has published over 1000 market intelligence reports in various markets / applications and served over 1,000 clients worldwide. This study is a culmination of four months of full-time effort performed by Lucintel's analyst team. The analysts used the following sources for the creation and completion of this valuable report:

- In-depth interviews of the major players in this market

- Detailed secondary research from competitors' financial statements and published data

- Extensive searches of published works, market, and database information pertaining to industry news, company press releases, and customer intentions

- A compilation of the experiences, judgments, and insights of Lucintel's professionals, who have analyzed and tracked this market over the years.

Extensive research and interviews are conducted across the supply chain of this market to estimate market share, market size, trends, drivers, challenges, and forecasts. Below is a brief summary of the primary interviews that were conducted by job function for this report.

Thus, Lucintel compiles vast amounts of data from numerous sources, validates the integrity of that data, and performs a comprehensive analysis. Lucintel then organizes the data, its findings, and insights into a concise report designed to support the strategic decision-making process. The figure below is a graphical representation of Lucintel's research process.

Buy Now

Choose a license that fits your team. Instant PDF delivery.

Prices exclude taxes. Instant delivery. Custom licensing available on request.

Frequently Asked Questions

What is the polyimide film market size?

What is the growth forecast for polyimide film market?

What are the major drivers influencing the growth of the polyimide film market?

What are the major segments for polyimide film market?

Who are the key polyimide film market companies?

Some of the key polyimide film companies are as follows:

- DuPont

- PI Advanced Materials Co. Ltd.

- Toray Industries

- Kaneka Corporation

- Ube Industries

- Taimide Tech. Inc.

- Arakawa Chemicals Industries

Which polyimide film market segment will be the largest in future?

In polyimide film market, which region is expected to be the largest in next 8 years?

Do we receive customization in this report?

Key Questions

- • What are some of the most promising, high-growth opportunities for the polyimide film market by application (flexible printed circuits, specialty fabricated products, pressure sensitive tape, wire & cable, and motor/generator), end use (electronics, automotive, aerospace, labeling, and others), and region (North America, Europe, Asia Pacific, and the Rest of the World)?

- • Which segments will grow at a faster pace and why?

- • Which region will grow at a faster pace and why?

- • What are the key factors affecting market dynamics? What are the key challenges and business risks in this market?

- • What are the business risks and competitive threats in this market?

- • What are the emerging trends in this market and the reasons behind them?

- • What are some of the changing demands of customers in the market?

- • What are the new developments in the market? Which companies are leading these developments?

- • Who are the major players in this market? What strategic initiatives are key players pursuing for business growth?

- • What are some of the competing products in this market and how big of a threat do they pose for loss of market share by material or product substitution?

- • What M&A activity has occurred in the last 7 years and what has its impact been on the industry?