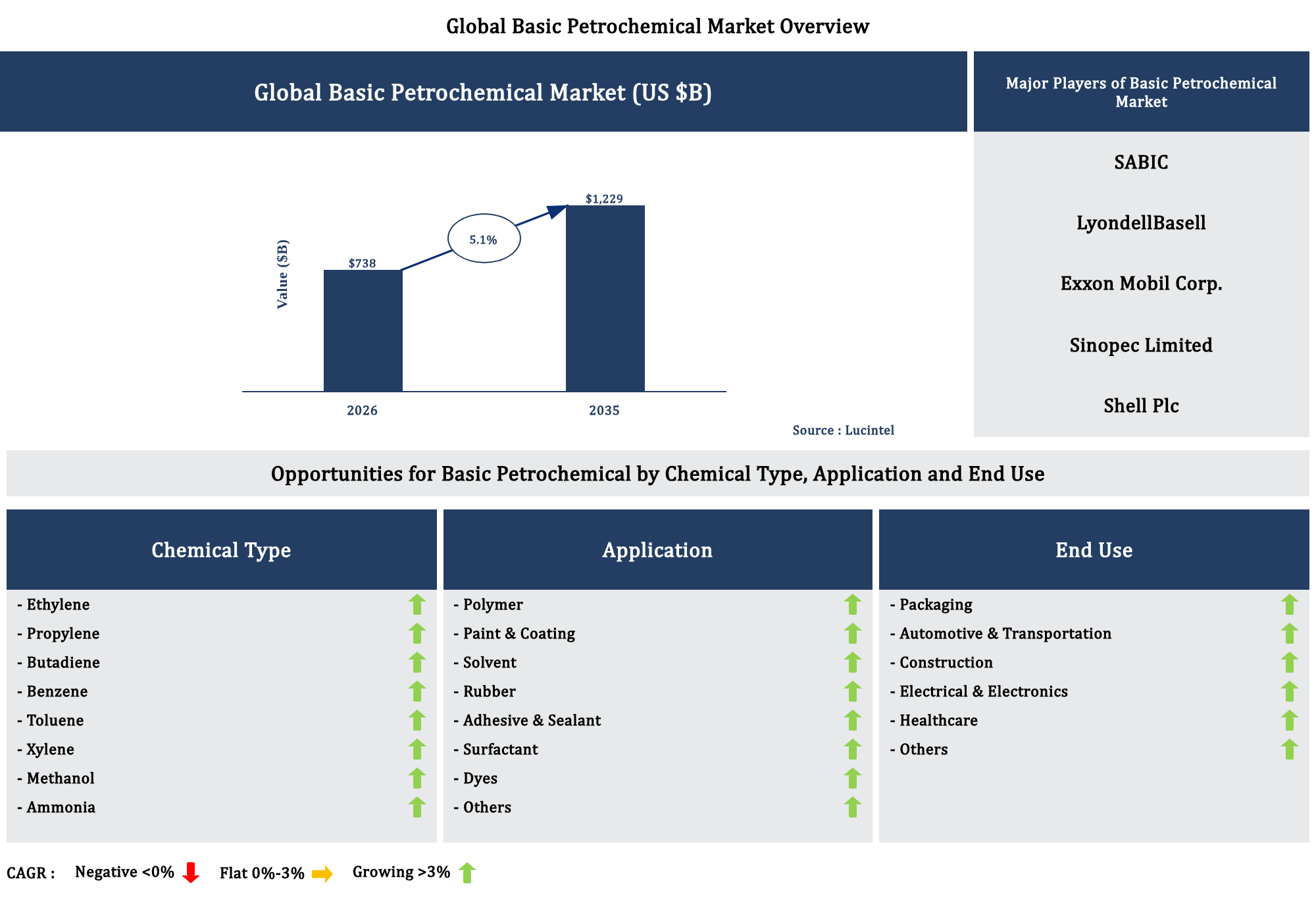

Basic Petrochemical Market

The future of the global basic petrochemical market looks promising with opportunities in the packaging, automotive & transportation, construction, electrical & electronic, and healthcare markets. The global basic petrochemical market is expected to reach an estimated $1,229 billion by 2035 with a CAGR of 5.1% from 2026 to 2035. The major drivers for this market are the increasing demand for plastics in packaging & consumer goods, the rising demand for synthetic fibers in textile industry, and the growing demand for petrochemicals in agriculture fertilizers.

Gain valuable insights for your business decisions with our comprehensive 150+ page report. Sample figures with some insights are shown below.

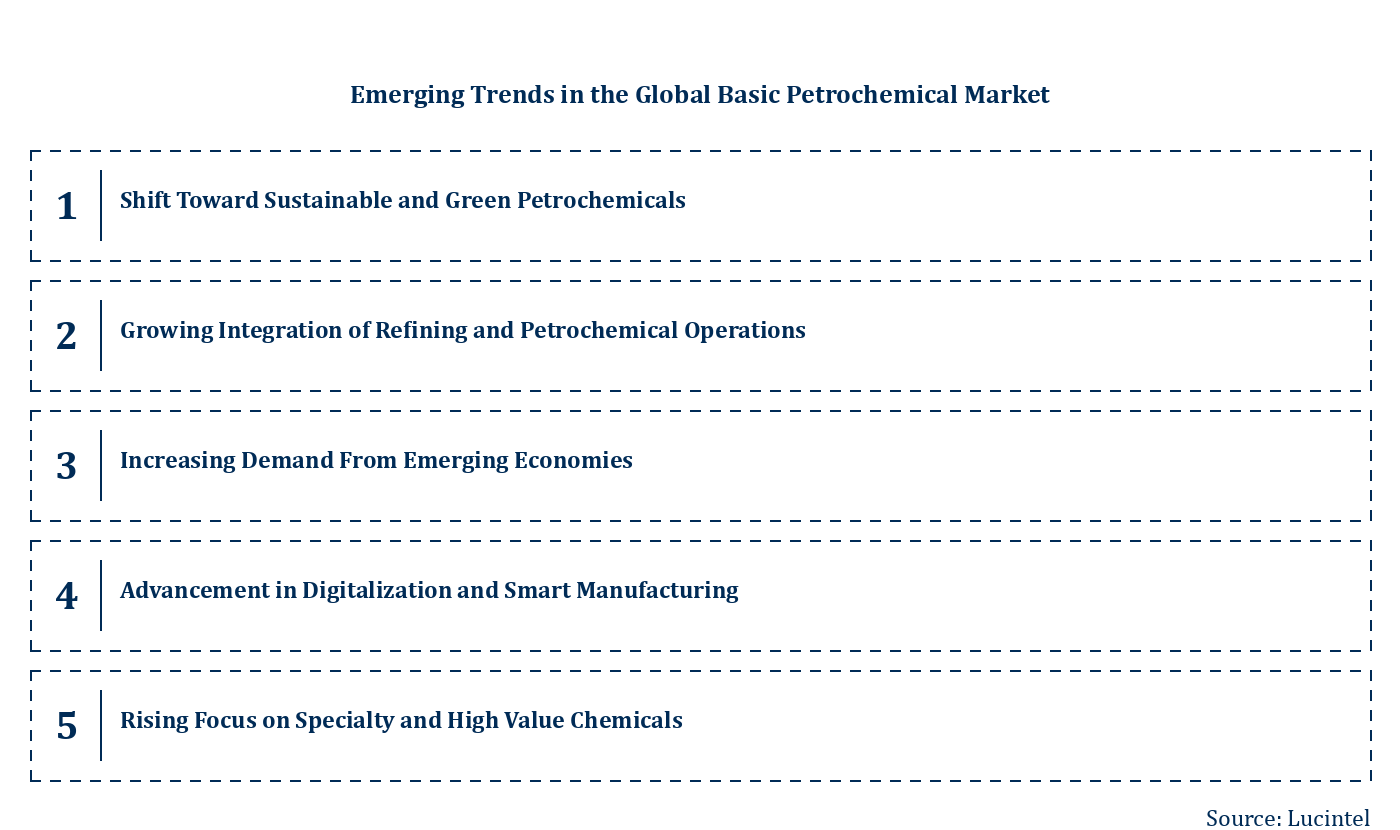

Emerging Trends in the Basic Petrochemical Market

The basic petrochemical market is evolving rapidly as global industries shift toward sustainability, efficiency, and advanced material demand. Changing feedstock dynamics, environmental regulations, and technological innovation are reshaping production and consumption patterns. Emerging economies are driving demand growth, while mature markets are focusing on value addition and carbon reduction. At the same time, digitalization and circular economy practices are transforming operational models across the value chain. These factors are creating new opportunities as well as challenges for market participants, influencing investment priorities, supply chain strategies, and long term competitiveness in the global petrochemical landscape.

These emerging trends are fundamentally reshaping the basic petrochemical market by driving sustainability, efficiency, and innovation. The shift toward green production, increased integration, and rising demand from emerging economies are redefining growth strategies. At the same time, digital transformation and the move toward specialty chemicals are enhancing competitiveness and profitability. Together, these trends are creating a more dynamic and resilient market landscape, where companies must continuously adapt to technological advancements, regulatory changes, and evolving consumer demands to maintain their position in the global petrochemical industry.

Recent Developments in the Basic Petrochemical Market

The basic petrochemical market is witnessing dynamic changes driven by evolving demand patterns, technological advancements, and sustainability initiatives. Industry players are focusing on capacity expansion, integration, and innovation to remain competitive in a changing global landscape. Governments and corporations are investing in infrastructure and cleaner technologies, while supply chain realignments are influencing trade flows. These developments are shaping production strategies and long term growth, creating new opportunities and challenges for stakeholders across the global petrochemical value chain.

These recent developments are significantly reshaping the basic petrochemical market by enhancing efficiency, sustainability, and competitiveness. Integration and digitalization are improving operational performance, while circular economy practices and bio based feedstocks are supporting environmental goals. At the same time, capacity rationalization and strategic investments are helping companies adapt to shifting demand patterns. Collectively, these changes are creating a more resilient and innovative market environment, where companies must continuously evolve to capture growth opportunities and maintain long term success in a competitive global landscape.

Strategic Growth Opportunities in the Basic Petrochemical Market

The basic petrochemical market is experiencing steady growth driven by rising demand across diverse end use applications such as packaging, automotive, construction, electronics, and healthcare. Increasing industrialization, urban expansion, and technological advancements are creating new avenues for petrochemical consumption. Companies are focusing on innovation, capacity expansion, and sustainability to capitalize on evolving market needs. These dynamics are opening strategic growth opportunities across key applications, enabling stakeholders to enhance value creation, improve competitiveness, and address changing consumer and regulatory expectations in the global petrochemical landscape.

The Strategic growth opportunities across key applications are significantly shaping the basic petrochemical market by driving demand and innovation. Packaging, automotive, construction, electronics, and healthcare sectors are creating strong avenues for expansion. These opportunities are encouraging investments in advanced materials, sustainable solutions, and capacity development. As industries continue to evolve, petrochemical companies are adapting to meet changing requirements and regulatory standards. Overall, these application driven opportunities are strengthening market growth, enhancing competitiveness, and ensuring long term value creation across the global petrochemical industry.

Basic Petrochemical Market Drivers and Challenges

The basic petrochemical market is influenced by a complex combination of technological, economic, and regulatory factors that shape its growth trajectory. Increasing demand from end use industries, advancements in production technologies, and expanding global trade are driving market expansion. At the same time, environmental regulations, fluctuating raw material prices, and supply chain disruptions present significant challenges. Companies must continuously adapt to these evolving dynamics by investing in innovation, improving efficiency, and aligning with sustainability goals. Understanding these drivers and challenges is essential for stakeholders to navigate uncertainties and capitalize on emerging opportunities in the global petrochemical landscape.

The factors responsible for driving the basic petrochemical market include:-

The challenges in the basic petrochemical market are:

The basic petrochemical market is shaped by a dynamic interplay of strong growth drivers and significant challenges. Rising demand from key industries, technological advancements, and expanding industrialization are fueling market growth and creating new opportunities. At the same time, environmental regulations, raw material price volatility, and competitive pressures are posing obstacles to sustained expansion. Companies must adopt innovative strategies, invest in sustainable solutions, and enhance operational efficiency to navigate these challenges. Overall, the balance between these drivers and challenges will determine the future growth, resilience, and competitiveness of the global petrochemical market.

List of Basic Petrochemical Market Companies

Companies in the market compete on the basis of product quality offered. Major players in this market focus on expanding their manufacturing facilities, R&D investments, infrastructural development, and leverage integration opportunities across the value chain. Through these strategies basic petrochemical market companies cater increasing demand, ensure competitive effectiveness, develop innovative products & technologies, reduce production costs, and expand their customer base. Some of the basic petrochemical market companies profiled in this report include-

Basic Petrochemical Market by Segment

The study includes a forecast for the global basic petrochemical market by chemical type, application, end use, and region.

Country Wise Outlook for the Basic Petrochemical Market

The basic petrochemical market is undergoing significant transformation globally, driven by capacity expansions, trade realignments, sustainability pressures, and shifting demand patterns. Major economies are focusing on increasing production efficiency, integrating refining with petrochemicals, and strengthening domestic supply chains. At the same time, geopolitical tensions, energy transitions, and environmental regulations are influencing investment decisions and operational strategies. Emerging economies are expanding capacity to meet rising demand, while mature markets are consolidating operations to remain competitive. These developments are reshaping global supply dynamics, trade flows, and long term growth prospects across the United States, China, Germany, India, and Japan.

Features of the Basic Petrochemical Market

Top 5 Companies

Table of Contents

List of Figures

List of Tables

Methodology

Lucintel has been in the business of market research and management consulting since 2000 and has published over 1000 market intelligence reports in various markets / applications and served over 1,000 clients worldwide. This study is a culmination of four months of full-time effort performed by Lucintel's analyst team. The analysts used the following sources for the creation and completion of this valuable report:

- In-depth interviews of the major players in this market

- Detailed secondary research from competitors' financial statements and published data

- Extensive searches of published works, market, and database information pertaining to industry news, company press releases, and customer intentions

- A compilation of the experiences, judgments, and insights of Lucintel's professionals, who have analyzed and tracked this market over the years.

Extensive research and interviews are conducted across the supply chain of this market to estimate market share, market size, trends, drivers, challenges, and forecasts. Below is a brief summary of the primary interviews that were conducted by job function for this report.

Thus, Lucintel compiles vast amounts of data from numerous sources, validates the integrity of that data, and performs a comprehensive analysis. Lucintel then organizes the data, its findings, and insights into a concise report designed to support the strategic decision-making process. The figure below is a graphical representation of Lucintel's research process.

Buy Now

Choose a license that fits your team. Instant PDF delivery.

Prices exclude taxes. Instant delivery. Custom licensing available on request.

Frequently Asked Questions

What is the basic petrochemical market size?

What is the growth forecast for basic petrochemical market?

What are the major drivers influencing the growth of the basic petrochemical market?

What are the major segments for basic petrochemical market?

Who are the key basic petrochemical market companies?

Some of the key basic petrochemical companies are as follows:

- SABIC

- LyondellBasell

- Exxon Mobil Corp.

- Sinopec Limited

- Shell Plc

Which basic petrochemical market segment will be the largest in future?

In basic petrochemical market, which region is expected to be the largest in next 8 years?

Do we receive customization in this report?

Key Questions

- • What are some of the most promising, high-growth opportunities for the basic petrochemical market by chemical type (ethylene, propylene, butadiene, benzene, toluene, xylene, methanol, and ammonia), application (polymer, paint & coating, solvent, rubber, adhesive & sealant, surfactant, dyes, and others), end use (packaging, automotive & transportation, construction, electrical & electronics, healthcare, and others), and region (North America, Europe, Asia Pacific, and the Rest of the World)?

- • Which segments will grow at a faster pace and why?

- • Which region will grow at a faster pace and why?

- • What are the key factors affecting market dynamics? What are the key challenges and business risks in this market?

- • What are the business risks and competitive threats in this market?

- • What are the emerging trends in this market and the reasons behind them?

- • What are some of the changing demands of customers in the market?

- • What are the new developments in the market? Which companies are leading these developments?

- • Who are the major players in this market? What strategic initiatives are key players pursuing for business growth?

- • What are some of the competing products in this market and how big of a threat do they pose for loss of market share by material or product substitution?

- • What M&A activity has occurred in the last 5 years and what has its impact been on the industry?