Satellite Solar Cell Material Market

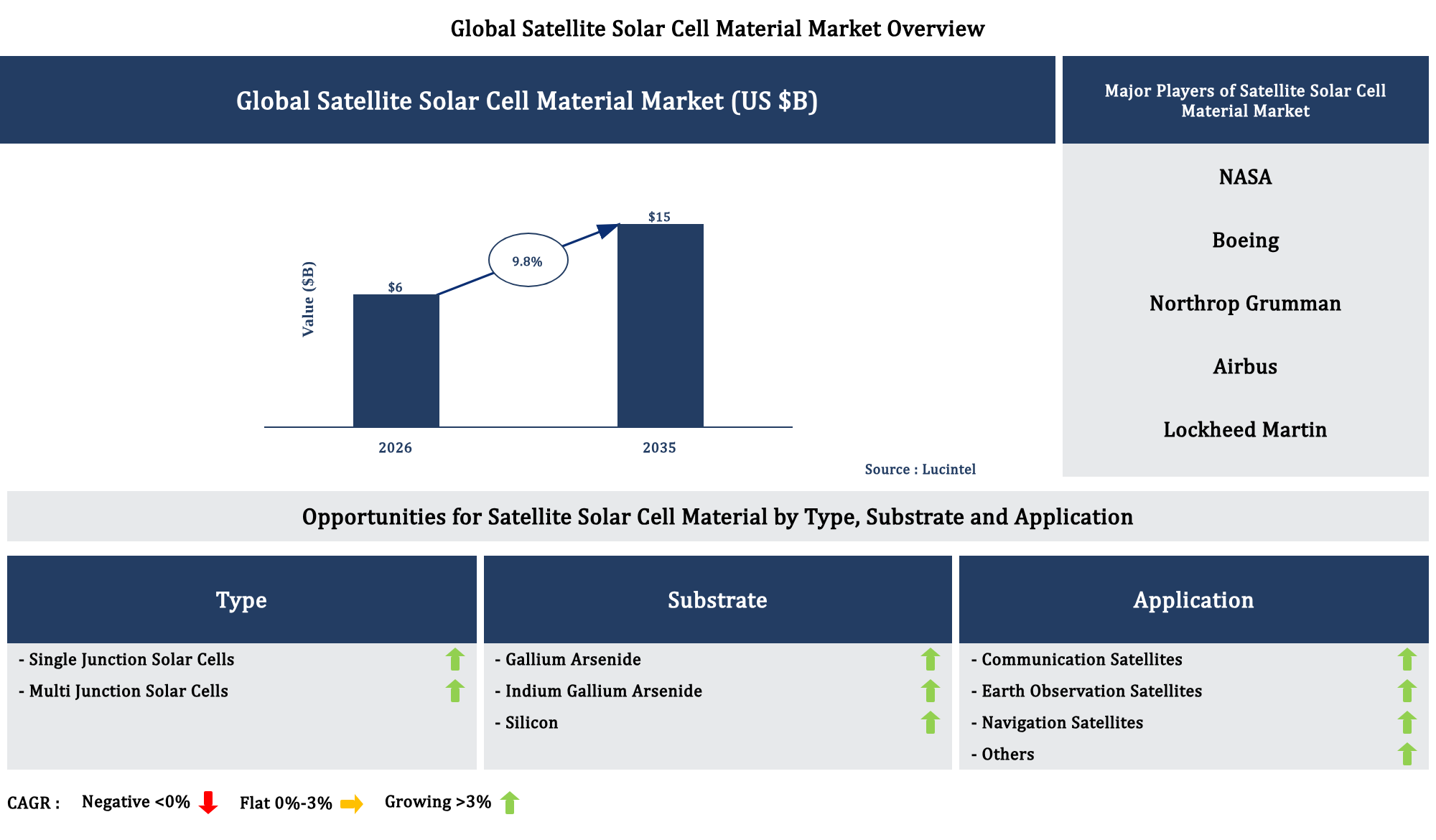

The future of the global satellite solar cell material market looks promising with opportunities in the communication satellite, earth observation satellite, and navigation satellite markets. The global satellite solar cell material market is expected to reach an estimated $15 billion by 2035 with a CAGR of 9.8% from 2026 to 2035. The major drivers for this market are the increasing demand for high-efficiency solar cells, the rising focus on lightweight satellite components, and the growing adoption of advanced photovoltaic materials.

Gain valuable insights for your business decisions with our comprehensive 150+ page report. Sample figures with some insights are shown below.

Emerging Trends in the Satellite Solar Cell Material Market

The satellite solar cell material market is experiencing rapid evolution driven by technological advancements, increasing demand for sustainable energy solutions, and the expanding satellite industry. As space exploration and satellite deployment grow, the need for efficient, lightweight, and durable solar cell materials becomes critical. Market players are investing in research to develop materials that can withstand harsh space conditions while maximizing energy output. These developments are not only enhancing satellite performance but also opening new avenues for commercial and governmental applications. The following trends highlight the key developments shaping this dynamic market landscape.

These trends are collectively transforming the satellite solar cell material market by improving efficiency, durability, and versatility. They are enabling more ambitious satellite missions, reducing costs, and supporting the growth of new space industries. As these developments continue, the market is poised for significant expansion, driven by technological innovation and increasing global space activity.

Recent Developments in the Satellite Solar Cell Material Market

The satellite solar cell material market is experiencing rapid advancements driven by increasing demand for sustainable energy solutions in space technology. Innovations in material efficiency, durability, and cost reduction are shaping the future of satellite power systems. As space exploration and satellite deployment expand, the market is poised for significant growth. These developments are not only enhancing satellite performance but also opening new opportunities for commercial and governmental space missions, making the market more competitive and technologically advanced.

The overall impact of these developments is a more efficient, durable, and cost-effective satellite solar cell market. These innovations are enabling longer missions, reducing costs, and expanding application possibilities, which collectively drive market growth. As technology continues to evolve, the satellite solar cell market is poised for significant expansion, supporting the increasing demand for space-based energy solutions and satellite deployment worldwide.

Strategic Growth Opportunities in the Satellite Solar Cell Material Market

The satellite solar cell material market is experiencing rapid growth driven by increasing demand for space exploration, satellite deployment, and renewable energy solutions. Advancements in material technology, miniaturization of satellites, and the need for high-efficiency solar cells are fueling market expansion. Strategic investments by government agencies and private companies are also contributing to innovation and market competitiveness. This evolving landscape presents numerous opportunities for stakeholders to capitalize on emerging applications and technological breakthroughs, ensuring sustained growth and market dominance.

The overall impact of these opportunities is set to significantly enhance the satellite solar cell material market, fostering innovation, reducing costs, and enabling more ambitious space missions. As technological advancements continue, stakeholders will benefit from increased market share and the ability to meet the evolving demands of space and terrestrial applications, ensuring sustained growth and competitiveness in this dynamic industry.

Satellite Solar Cell Material Market Drivers and Challenges

The satellite solar cell material market is influenced by a variety of technological, economic, and regulatory factors that shape its growth trajectory. Advances in solar cell efficiency, material innovation, and manufacturing processes drive market expansion. Economic considerations such as decreasing costs of solar technology and increasing demand for sustainable energy solutions further propel growth. Regulatory policies promoting renewable energy adoption and environmental standards also play a crucial role. However, the market faces challenges including technological limitations, high production costs, and regulatory hurdles that could impede progress. Understanding these drivers and challenges is essential for stakeholders to navigate the evolving landscape effectively.

The factors responsible for driving the satellite solar cell material market include:-

The challenges facing the satellite solar cell material market include:-

The satellite solar cell material market is driven by technological advancements, cost reductions, industry growth, and supportive policies, which collectively foster expansion and innovation. However, technological limitations, high costs, and regulatory uncertainties pose significant hurdles that could slow progress. The overall impact of these drivers and challenges will shape the future landscape, requiring stakeholders to focus on innovation, cost management, and regulatory compliance to capitalize on emerging opportunities and sustain growth in this dynamic market.

List of Satellite Solar Cell Material Market Companies

Companies in the market compete on the basis of product quality offered. Major players in this market focus on expanding their manufacturing facilities, R&D investments, infrastructural development, and leverage integration opportunities across the value chain. Through these strategies satellite solar cell material market companies cater increasing demand, ensure competitive effectiveness, develop innovative products & technologies, reduce production costs, and expand their customer base. Some of the satellite solar cell material market companies profiled in this report include-

Satellite Solar Cell Material Market by Segment

The study includes a forecast for the global satellite solar cell material market by type, substrate, application, and region.

Country Wise Outlook for the Satellite Solar Cell Material Market

The satellite solar cell material market is experiencing rapid growth driven by increasing demand for space exploration, satellite technology, and renewable energy sources. Advances in material science, manufacturing processes, and international collaborations are shaping the future of this industry. Countries are investing heavily in research and development to enhance the efficiency, durability, and cost-effectiveness of solar cell materials for satellite applications. These developments are crucial for supporting the expanding satellite networks, space missions, and sustainable energy initiatives worldwide. The following summarizes recent key developments in this market across the United States, China, Germany, India, and Japan.

Features of the Satellite Solar Cell Material Market

Top 5 Companies

Table of Contents

List of Figures

List of Tables

Methodology

Lucintel has been in the business of market research and management consulting since 2000 and has published over 1000 market intelligence reports in various markets / applications and served over 1,000 clients worldwide. This study is a culmination of four months of full-time effort performed by Lucintel's analyst team. The analysts used the following sources for the creation and completion of this valuable report:

- In-depth interviews of the major players in this market

- Detailed secondary research from competitors' financial statements and published data

- Extensive searches of published works, market, and database information pertaining to industry news, company press releases, and customer intentions

- A compilation of the experiences, judgments, and insights of Lucintel's professionals, who have analyzed and tracked this market over the years.

Extensive research and interviews are conducted across the supply chain of this market to estimate market share, market size, trends, drivers, challenges, and forecasts. Below is a brief summary of the primary interviews that were conducted by job function for this report.

Thus, Lucintel compiles vast amounts of data from numerous sources, validates the integrity of that data, and performs a comprehensive analysis. Lucintel then organizes the data, its findings, and insights into a concise report designed to support the strategic decision-making process. The figure below is a graphical representation of Lucintel's research process.

Buy Now

Choose a license that fits your team. Instant PDF delivery.

Prices exclude taxes. Instant delivery. Custom licensing available on request.

Frequently Asked Questions

What is the satellite solar cell material market size?

What is the growth forecast for satellite solar cell material market?

What are the major drivers influencing the growth of the satellite solar cell material market?

What are the major segments for satellite solar cell material market?

Who are the key satellite solar cell material market companies?

Some of the key satellite solar cell material companies are as follows:

- NASA

- Boeing

- Northrop Grumman

- Airbus

- Lockheed Martin

- Thales Alenia Space

- Maxar Technologies

- JAXA

- China Aerospace Corporation

- SHARP CORPORATION

Which satellite solar cell material market segment will be the largest in future?

In satellite solar cell material market, which region is expected to be the largest in next 8 years?

Do we receive customization in this report?

Key Questions

- • What are some of the most promising, high-growth opportunities for the satellite solar cell material market by type (single junction solar cells and multi junction solar cells), substrate (gallium arsenide, indium gallium arsenide, and silicon), application (communication satellites, earth observation satellites, navigation satellites, and others), and region (North America, Europe, Asia Pacific, and the Rest of the World)?

- • Which segments will grow at a faster pace and why?

- • Which region will grow at a faster pace and why?

- • What are the key factors affecting market dynamics? What are the key challenges and business risks in this market?

- • What are the business risks and competitive threats in this market?

- • What are the emerging trends in this market and the reasons behind them?

- • What are some of the changing demands of customers in the market?

- • What are the new developments in the market? Which companies are leading these developments?

- • Who are the major players in this market? What strategic initiatives are key players pursuing for business growth?

- • What are some of the competing products in this market and how big of a threat do they pose for loss of market share by material or product substitution?

- • What M&A activity has occurred in the last 5 years and what has its impact been on the industry?