Metal Coil Lamination Market

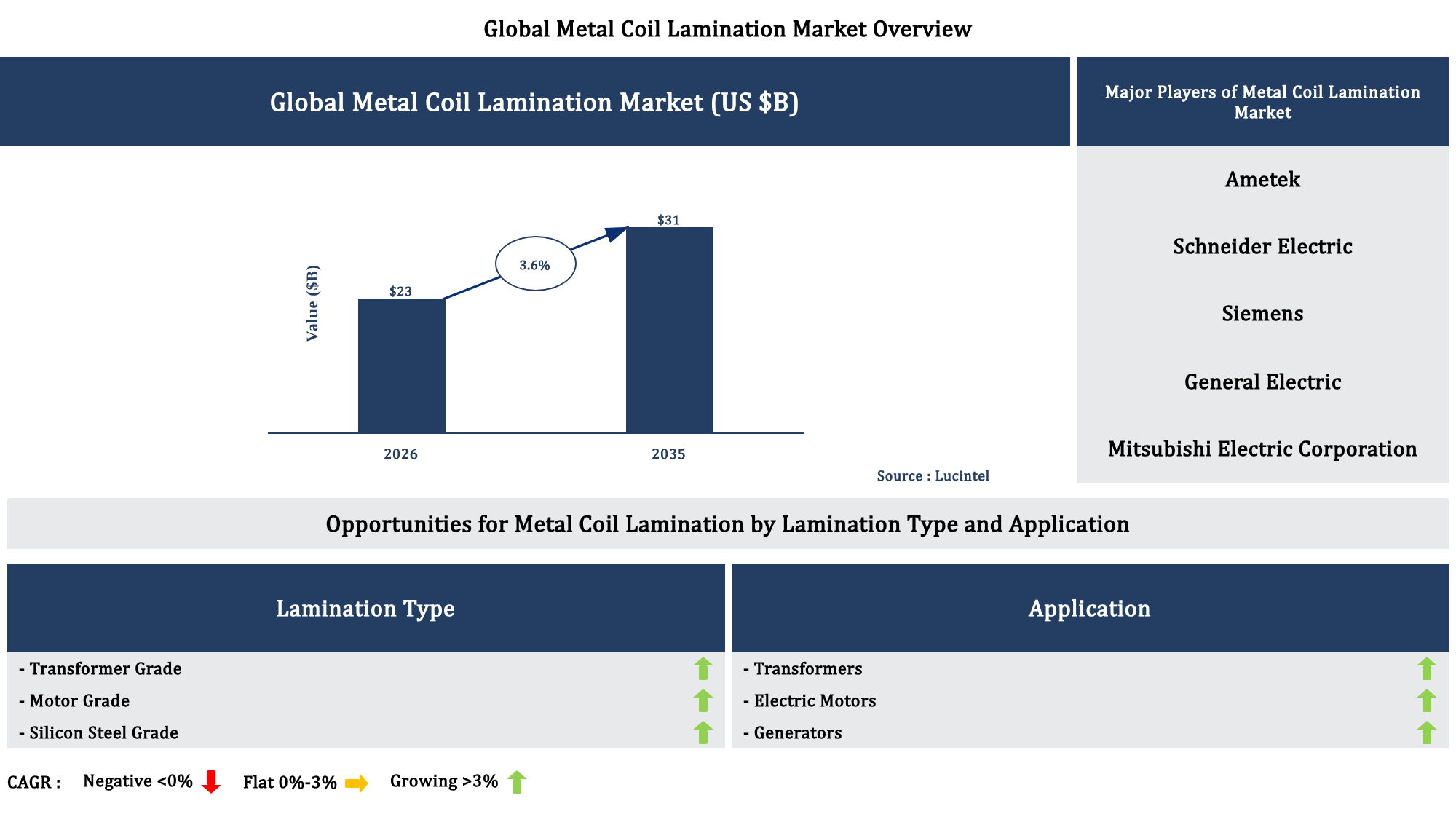

The future of the global metal coil lamination market looks promising with opportunities in the transformers, electric motors and generators markets. The global metal coil lamination market is expected to reach an estimated $31 billion by 2035 with a CAGR of 3.6% from 2026 to 2035. The major drivers for this market are the increasing demand for durable building materials, the rising adoption in appliance manufacturing and the growing use across construction applications.

• Lucintel forecasts that, within the lamination type category, transformer grade will remain the largest segment over the forecast period as the high demand in power generation & distribution industries.

• Within the application category, transformers will remain the largest segment due to the the essential role in electricity distribution & regulation.

• In terms of regions, North America will remain the largest region over the forecast period due to the the increasing demand from the automotive & electronics sectors.

Gain valuable insights for your business decisions with our comprehensive 150+ page report.

Emerging Trends in the Metal Coil Lamination Market

The metal coil lamination market is evolving rapidly as manufacturers, converters, and end-use industries seek higher functional performance, lighter weights, and more sustainable material solutions. Advances in coatings, adhesives, and surface engineering are enabling laminated metal coils to deliver improved corrosion resistance, decorative appeal, barrier properties, and formability across automotive, construction, packaging, and appliance applications. At the same time, digitalization and automation are reshaping how coils are specified, produced, and quality-controlled. These emerging trends are redefining competitive dynamics, pushing suppliers to innovate faster while meeting stricter regulatory, environmental, and cost-efficiency requirements across global value chains.

Recent Developments in the Metal Coil Lamination Market

The metal coil lamination market has entered a phase of accelerated transformation as manufacturers, OEMs, and end-use industries demand higher performance, greater design flexibility, and stronger sustainability credentials. Advances in coating chemistries, digital manufacturing, and automation are reshaping how laminated coils are produced, specified, and integrated into applications ranging from construction and appliances to automotive and packaging. At the same time, supply chain shocks and evolving regulatory frameworks are compelling stakeholders to rethink sourcing strategies and material choices. The following recent developments illustrate how the metal coil lamination market is evolving to meet these multidimensional pressures.

Strategic Growth Opportunities in the Metal Coil Lamination Market

The metal coil lamination market is entering a phase of strategic expansion as manufacturers seek higher performance, durability, and sustainability across end-use sectors. Rising demand for lightweight structures, corrosion protection, and aesthetic finishes is reshaping expectations for laminated metal coils in automotive, construction, consumer goods, electronics, and industrial equipment. At the same time, stricter regulations on emissions, recyclability, and workplace safety are driving innovation in adhesive chemistries, surface treatments, and process automation. Companies that align product development with application-specific needs can unlock profitable niches, deepen customer partnerships, and secure long-term growth in the metal coil lamination market.

Metal Coil Lamination Market Drivers and Challenges

The global metal coil lamination market is influenced by a multifaceted set of technological, economic, and regulatory factors that collectively shape growth trajectories and competitive dynamics. Advancements in surface engineering, adoption of high-performance polymers and adhesives, and automation in coil processing are expanding application possibilities across construction, automotive, appliances, and industrial equipment. At the same time, volatility in raw material prices, tightening environmental regulations, and complex global supply chains introduce uncertainty and margin pressure. Stakeholders must understand how these drivers and challenges interact to optimize investment decisions, product portfolios, and geographic expansion strategies in this evolving market.

The factors responsible for driving the metal coil lamination market include:

The challenges facing this metal coil lamination market include:

The metal coil lamination market is shaped by a dynamic balance between robust growth drivers and persistent structural challenges. Expanding construction, automotive, and appliance demand, combined with aesthetic, durability, and sustainability requirements, is propelling wider adoption of laminated coils across regions and applications. At the same time, raw material volatility, capital intensity, and competition from other finishing technologies pressure margins and complicate strategic planning. Success in this market depends on technological innovation, disciplined cost management, and close collaboration across the value chain. Companies that effectively leverage these drivers while mitigating the challenges are positioned to capture sustainable, long-term growth opportunities.

List of Metal Coil Lamination Market Companies

Companies in the market compete on the basis of product quality offered. Major players in this market focus on expanding their manufacturing facilities, R&D investments, infrastructural development, and leverage integration opportunities across the value chain. Through these strategies metal coil lamination market companies cater increasing demand, ensure competitive effectiveness, develop innovative products & technologies, reduce production costs, and expand their customer base. Some of the metal coil lamination market companies profiled in this report include-

Metal Coil Lamination Market by Segment

The study includes a forecast for the global metal coil lamination market by lamination type, application, and region.

Country Wise Outlook for the Metal Coil Lamination Market

The metal coil lamination market is evolving quickly as manufacturers seek higher performance, lighter weight, and more sustainable solutions for automotive, construction, appliances, and electrical infrastructure. Across major economies, innovation is concentrating on advanced coatings, improved corrosion resistance, energy-efficient production, and integration with digital manufacturing. Environmental regulations, volatility in metal prices, and shifts in end-use sectors are reshaping how laminated coils are designed, specified, and sourced. In parallel, supply chain reconfiguration and regionalization are prompting new capacity investments and localization strategies. The following country snapshots highlight recent developments in the United States, China, Germany, India, and Japan.

Features of the Metal Coil Lamination Market

Article

Metal Coil Lamination Market: Are Advanced Laminates Re‑Engineering the Future of Industrial Materials?

Dallas, June 11, 2026 – The metal coil lamination market is undergoing a visible transformation as manufacturers, technology firms, and end users converge around higher-performance, lighter, and more sustainable laminated coils. From electric vehicles and high-efficiency motors to precision electronics and data center infrastructure, laminated metal coils are shifting from commodity inputs to strategic enablers of performance and cost competitiveness. The industry is being reshaped by new materials, process digitalization, and rising regulatory pressure on energy efficiency and carbon footprints, forcing producers and buyers to rethink sourcing, design, and partnership strategies.

How Are New Material Architectures and Hybrid Laminates Changing Market Dynamics?

A key trend in the metal coil lamination market centers on multi-material and hybrid laminate architectures that combine metals with polymers, adhesives, and functional coatings tailored to specific performance needs. Manufacturers are moving beyond traditional steel-only stacks toward laminations that integrate aluminum, advanced steels, copper alloys, specialty films, and nano-engineered coatings. This shift is particularly disruptive for markets such as automotive, consumer electronics, and building systems where weight, corrosion resistance, noise reduction, and electrical performance directly influence product value and compliance with emerging standards.

Another trend is the push toward ultra-thin gauge laminations with tighter tolerances and controlled surface finishes, supporting higher-frequency electrical applications and compact component footprints. In motor and transformer applications, finer lamination thickness reduces eddy current losses, enabling higher efficiency ratings that are increasingly mandated by policymakers. These material advances are also influencing supply chain structures, as end users are seeking closer collaboration with lamination specialists to co-design materials that fit proprietary technologies and long-term platform strategies.

In Which Markets Will Process Automation and Digitalization Create the Most Impact?

The metal coil lamination market is seeing rapid adoption of digital process control, advanced sensors, and AI-driven quality analytics. Automated slit-and-stack lines, laser cutting, and in-line inspection systems are allowing producers to deliver consistent performance at higher speeds while minimizing scrap. Automotive electrification is expected to be among the major beneficiaries, as electric vehicle platforms require precise, repeatable laminations for traction motors, onboard chargers, and power electronics. As platforms scale globally, automakers are demanding shorter development cycles, localized supply, and complete traceability, all of which favor producers that invest in digitalized lamination lines.

Data centers and power electronics markets are also poised to gain significantly from digital production capabilities. The continuous deployment of high-efficiency power supplies, uninterruptible power systems, and converters depends on reliable laminated cores that meet strict loss and thermal management specifications. By employing machine learning to correlate process parameters with magnetic and mechanical performance, lamination manufacturers can fine-tune recipes for different end uses, reducing lead times and enabling just-in-time fulfillment for technology customers that cannot afford line downtime.

Why Is Sustainability Becoming a Strategic Battleground in the metal coil lamination market?

Sustainability considerations are rapidly moving from marketing messages to hard procurement criteria, forcing the metal coil lamination market to respond with lower-carbon materials and more circular business models. Energy-intensive coil processing steps, such as annealing, coating, and slitting, are under scrutiny as customers pursue science-based climate targets and green financing. Producers are experimenting with bio-based or low-VOC adhesive systems, water-based coatings, and improved heat recovery on lines to reduce both emissions and operating costs. Such innovations are gaining traction in sectors where environmental declarations and lifecycle assessments are increasingly embedded into tender requirements.

At the same time, recyclability is turning into a differentiator. Laminations that are easier to disassemble and recycle help downstream manufacturers improve their own circularity metrics. Electric motor and transformer producers are beginning to evaluate laminates not only on performance and price but also on end-of-life recovery rates and alignment with extended producer responsibility regimes. This introduces opportunities for lamination specialists that can design products with standardized metal compositions, easily separable layers, and documented recycled content that satisfies new regulations and brand commitments.

What Challenges Threaten to Slow Adoption of Next-Generation Laminates?

Despite compelling innovation, the metal coil lamination market faces structural and operational headwinds that could slow or unevenly distribute adoption. Many advanced laminates require new coatings, adhesives, and precise thermal processing profiles, which involve upfront capital expenditure and learning curves that some mid-sized processors are reluctant to assume. In resource-constrained environments, buyers may default to established solutions, even when they sacrifice performance or sustainability benefits, especially if short-term price pressures dominate decision-making.

Another challenge is the persistent volatility in raw material prices and availability, particularly for specialty steels, copper, and engineered films. Producers must maintain multiple qualified material sources and design flexible production recipes to avoid bottlenecks, while still guaranteeing performance consistency. Geopolitical risks and trade restrictions are amplifying these concerns, prompting some buyers to regionalize lamination supply chains, potentially favoring players with multi-continent footprints and diversified sourcing strategies.

Where Do the Largest Opportunities Lie for Technology-Driven Use Cases?

Opportunities in the metal coil lamination market are increasingly concentrated around technology-driven applications that demand precision, reliability, and differentiated performance. In the technology industry, laminated magnetic cores are foundational components for transformers, inductors, and motors found in data centers, telecommunications networks, consumer devices, and industrial automation systems. The push toward higher power densities and miniaturization is creating demand for laminations that minimize core losses and manage heat without sacrificing mechanical stability.

Data centers relying on high-efficiency power supplies and backup systems represent a robust and growing use case. As operators optimize total cost of ownership and sustainability metrics, every percentage point improvement in transformer or inductor efficiency translates into sizable energy savings. Similarly, 5G network rollouts and edge computing infrastructure require compact, reliable magnetic components, spurring opportunities for lamination designs tuned to specific frequency ranges and thermal conditions. Consumer electronics, including high-end audio, gaming systems, and smart appliances, also rely on laminated cores where noise reduction, efficiency, and compact form factors drive competitive differentiation.

Which Recent Developments Signal the Next Phase of Market Disruption?

Recent activity in the metal coil lamination market highlights a convergence of materials science, process technology, and strategic partnerships. Major steel and specialty material suppliers are launching new grades tailored for high-frequency applications, such as electric vehicle motors and fast-switching power electronics, with improved magnetic properties and lower core losses. At the same time, lamination processors are investing in laser cutting and advanced punching technologies that reduce burr formation, enhance edge quality, and enable intricate geometries suited to compact, high-speed machines.

Digital twins and simulation tools are beginning to play a bigger role in how laminated stacks are designed and validated, allowing manufacturers and end users to collaborate virtually on new motor or transformer platforms before committing to tooling. Strategic alliances between lamination firms, motor designers, and power electronics companies are emerging to accelerate development cycles and ensure that new laminate solutions align with future product roadmaps. On the financial and corporate side, private equity and strategic buyers have increased their focus on specialized lamination assets, viewing them as critical nodes in the electrification and digital infrastructure value chains.

How Should Stakeholders Position Themselves as the metal coil lamination market Evolves?

As the metal coil lamination market continues to evolve, stakeholders across the value chain must treat laminations as strategic levers rather than interchangeable commodities. For end users in technology, automotive, and energy, closer collaboration with lamination partners will be essential to unlock differentiated performance, meet tightening efficiency regulations, and deliver on sustainability commitments. For producers, the competitive landscape will increasingly favor those that combine advanced materials capabilities with digitalized operations, resilient sourcing, and application-specific engineering support.

Companies that proactively invest in hybrid laminates, automation, sustainability, and collaborative design models are likely to capture disproportionate value as electrification, digitalization, and decarbonization accelerate. Those that delay modernization may find themselves relegated to low-margin segments, squeezed by both customers demanding more and innovators offering compelling alternatives. The metal coil lamination market is entering a phase where innovation in materials and processes is not optional but central to long-term competitiveness and relevance in the broader industrial and technology ecosystems.

Top 5 Companies

1. Ametek

Ametek is a diversified global manufacturer of electronic instruments and electromechanical devices with a meaningful role in equipment and components that interface with the metal coil lamination market. Headquartered in Berwyn, Pennsylvania and founded in 1930, the company employs tens of thousands of people across North America, Europe, and Asia, serving industrial, aerospace, power, and process markets. Within the metal coil lamination value chain, Ametek offers precision measurement instruments, automation and motion solutions, motors, and specialty materials that support coil processing, lamination cutting, and quality assurance in electrical steel and nonferrous laminates. Its product portfolio includes motors and blowers used in laminated-core machines, power quality and monitoring systems for lamination lines, and test and measurement equipment for coating thickness, surface characterization, and electrical properties of laminated coils. Ametek has expanded its global presence through manufacturing and service facilities in key industrial regions, often co-locating near major steel and electrical equipment clusters to support OEMs and tier suppliers in the metal coil and transformer industries. Recent geographic expansion has focused on strengthening its footprint in China, India, and other Asia-Pacific markets, where demand for motors, transformers, and other laminated-core devices is rising. Ametek routinely pursues acquisitions to broaden its niche instrumentation and electromechanical portfolio, several of which indirectly reinforce its offerings for coil lamination process control, industrial automation, and quality testing capabilities across global metal processing facilities.

2. Schneider Electric

Schneider Electric is a global leader in energy management and industrial automation, with solutions that heavily depend on metal coil laminations in transformers, motors, and low and medium voltage equipment. Based in Rueil-Malmaison, France and tracing its origins to 1836, the company employs well over 150,000 people and has operations in more than 100 countries. Schneider’s portfolio includes power distribution equipment, switchgear, transformers, drives, and motor control centers, all of which incorporate laminated steel cores and metal coil laminations for efficient electromagnetic performance. Through brands and platforms such as EcoStruxure, Schneider integrates digital control, automation hardware, and energy monitoring to optimize manufacturing lines used to process and assemble laminated coils. The company’s geographic presence spans Europe, North America, Asia-Pacific, Latin America, and the Middle East and Africa, with factories and engineering centers located near major electrosteel and transformer hubs that demand high-quality lamination technologies. Schneider continues to expand production and engineering capabilities in India, China, and Southeast Asia to cater to growing grid modernization and industrial electrification that drive metal coil lamination consumption. The company is also active in acquiring and partnering with automation, software, and power equipment firms, and these deals often enhance its ability to offer advanced drives, motors, and digital twins for equipment that uses laminated cores, thereby supporting higher efficiency standards in the global metal coil lamination market.

3. Siemens

Siemens is a leading global technology company focused on electrification, automation, and digitalization, and it is deeply embedded in value chains that rely on metal coil laminations for motors, generators, and transformers. Headquartered in Munich and founded in 1847, Siemens employs more than 300,000 people, with a strong presence across Europe, the Americas, Asia-Pacific, and the Middle East and Africa. Its portfolio spans industrial automation systems, drive technologies, power transmission and distribution equipment, and rail traction solutions, all of which require high-performance laminated steel cores and precision coil assemblies. For the metal coil lamination market, Siemens provides advanced motor and generator designs that demand premium electrical steel laminations, as well as automation, motion control, and digital simulation tools for lamination stamping, stacking, and insulation processes. The company’s geographic expansion continues in fast-growing regions such as India, China, and Southeast Asia, where Siemens sets up manufacturing, engineering, and service centers to support local production of motors, transformers, and renewable energy equipment built on laminated cores. In addition, Siemens invests heavily in digital twin and manufacturing execution systems that enable optimization of coil lamination production lines. The company has a long history of strategic mergers, divestments, and spin-offs, and while recent portfolio moves have concentrated on strengthening smart infrastructure and digital industries, they indirectly reinforce Siemens’ influence over specification, sourcing, and processing of metal coil laminations used in its installed base of industrial and energy equipment worldwide.

4. General Electric

General Electric is a diversified industrial and energy technology company whose businesses rely extensively on metal coil laminations for rotating machines, transformers, and power equipment. Headquartered in Boston and formed in 1892, GE maintains a global workforce of well over 100,000 employees across North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa. Its core segments, including power generation, renewable energy, aerospace, and grid solutions, use electrical steel laminations in generators, large motors, and transformers for thermal, hydro, wind, and grid infrastructure applications. GE’s product offerings influence specifications for high-grade grain-oriented and non-grain-oriented electrical steel, coating systems, and stacked lamination geometries that underpin performance and efficiency in the metal coil lamination market. The company has manufacturing plants, service centers, and engineering hubs around the world, notably in the United States, Europe, India, and China, supporting local sourcing and processing of laminated coils for turbines, industrial drives, and grid equipment. Recent geographic expansion in renewable energy, transmission, and distribution projects in Asia and the Middle East has driven demand for transformers and generators that depend on advanced lamination designs and processing capabilities. GE’s history of mergers, acquisitions, and portfolio restructuring, including deals in power and grid technology, has shaped its role in specifying and integrating laminated-core equipment. While corporate simplification has focused on core aerospace and energy-related businesses, GE remains a major global influencer of metal coil lamination requirements, partnering with material suppliers and fabricators to improve efficiency and reduce losses in its next-generation electrical machines.

5. Mitsubishi Electric Corporation

Mitsubishi Electric Corporation is a leading Japanese multinational specializing in electrical and electronic equipment, with strong exposure to sectors that utilize metal coil laminations, including factory automation, power systems, transportation, and HVAC. Established in 1921 and headquartered in Tokyo, the company employs tens of thousands of people across Japan, Asia-Pacific, Europe, and the Americas. Mitsubishi Electric manufactures motors, inverters, transformers, generators, and railway traction equipment, all of which rely on precision-engineered laminated cores and metal coil assemblies. In the metal coil lamination market, the company acts both as a major end user and as a technology driver, specifying high-efficiency electrical steel laminations, insulation coatings, and advanced manufacturing techniques to achieve low core loss and compact machine designs. Its global geographic presence includes production bases and R and D centers in Japan, China, Southeast Asia, Europe, and North America, enabling close collaboration with steel producers and lamination fabricators. Mitsubishi Electric has been expanding capacity and solutions for energy-efficient motors and inverters, particularly in Asia and Europe, supporting higher performance requirements for laminated cores in industrial machinery, elevators, and air conditioning systems. The company pursues targeted acquisitions and partnerships in factory automation, power electronics, and transportation, which indirectly strengthen its role in driving innovation in metal coil lamination design and processing methodologies. By combining advanced materials, precision manufacturing, and control electronics, Mitsubishi Electric helps shape global standards and demand patterns in the metal coil lamination market.

Table of Contents

List of Figures

List of Tables

Methodology

Lucintel has been in the business of market research and management consulting since 2000 and has published over 1000 market intelligence reports in various markets / applications and served over 1,000 clients worldwide. This study is a culmination of four months of full-time effort performed by Lucintel's analyst team. The analysts used the following sources for the creation and completion of this valuable report:

- In-depth interviews of the major players in this market

- Detailed secondary research from competitors' financial statements and published data

- Extensive searches of published works, market, and database information pertaining to industry news, company press releases, and customer intentions

- A compilation of the experiences, judgments, and insights of Lucintel's professionals, who have analyzed and tracked this market over the years.

Extensive research and interviews are conducted across the supply chain of this market to estimate market share, market size, trends, drivers, challenges, and forecasts. Below is a brief summary of the primary interviews that were conducted by job function for this report.

Thus, Lucintel compiles vast amounts of data from numerous sources, validates the integrity of that data, and performs a comprehensive analysis. Lucintel then organizes the data, its findings, and insights into a concise report designed to support the strategic decision-making process. The figure below is a graphical representation of Lucintel's research process.

Buy Now

Choose a license that fits your team. Instant PDF delivery.

Prices exclude taxes. Instant delivery. Custom licensing available on request.

Frequently Asked Questions

What is the Metal Coil Lamination Market size?

What is the growth forecast for Metal Coil Lamination Market?

What are the major drivers influencing the growth of the Metal Coil Lamination Market?

What are the major segments for Metal Coil Lamination Market?

Who are the key Metal Coil Lamination Market companies?

Which Metal Coil Lamination Market segment will be the largest in future?

In Metal Coil Lamination Market, which region is expected to be the largest in next 9 years?

Do we receive customization in this report?

Key Questions

- • What are some of the most promising, high-growth opportunities for the Metal Coil Lamination Market by Lamination Type (Transformer Grade, Motor Grade, and Silicon Steel Grade), Application (Transformers, Electric Motors, and Generators), and region (North America, Europe, Asia Pacific, and the Rest of the World)?

- • Which segments will grow at a faster pace and why?

- • Which region will grow at a faster pace and why?

- • What are the key factors affecting market dynamics? What are the key challenges and business risks in this market?

- • What are the business risks and competitive threats in this market?

- • What are the emerging trends in this market and the reasons behind them?

- • What are some of the changing demands of customers in the market?

- • What are the new developments in the market? Which companies are leading these developments?

- • Who are the major players in this market? What strategic initiatives are key players pursuing for business growth?

- • What are some of the competing products in this market and how big of a threat do they pose for loss of market share by material or product substitution?

- • What M&A activity has occurred in the last 9 years, and what has its impact been on the industry?