Phase Change Material Market

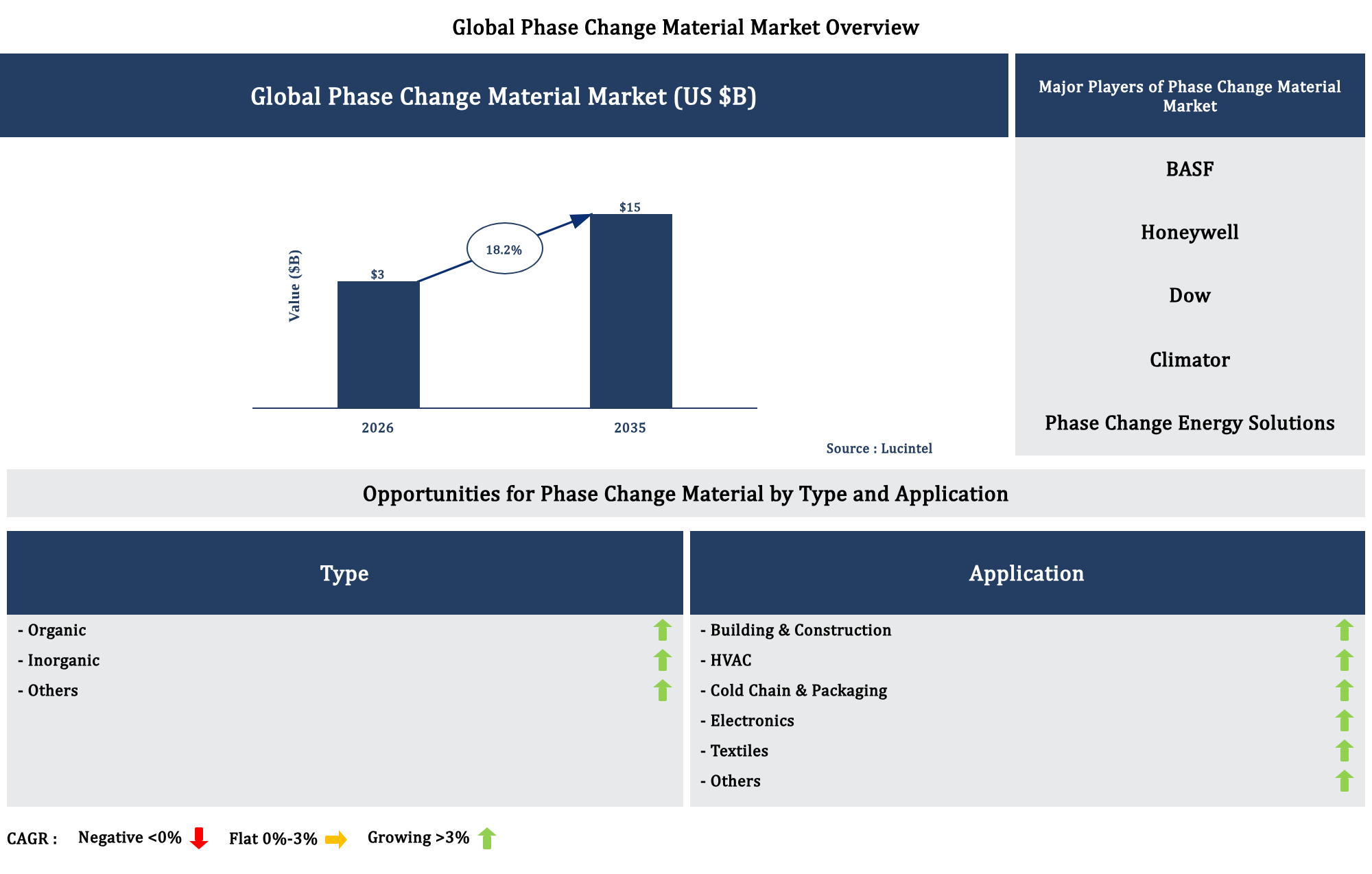

The future of the global phase change material market looks promising with opportunities in the building & construction, HVAC, cold chain & packaging, electronics and textiles markets. The global phase change material market is expected to reach an estimated $15 billion by 2035 with a CAGR of 18.2% from 2026 to 2035. The major drivers for this market are the increasing demand for energy-efficient buildings, the rising adoption of thermal energy storage and the growing use in temperature-sensitive applications.

• Lucintel forecasts that, within the type category, organic will remain the largest segment over the forecast period as the increasing demand for sustainable thermal storage solutions.

• Within the application category, building & construction will remain the largest segment due to the the growing adoption of energy-efficient building materials.

• In terms of regions, North America will remain the largest region over the forecast period due to the the increasing adoption of energy efficient building solutions.

Gain valuable insights for your business decisions with our comprehensive 150+ page report.

Emerging Trends in the Phase Change Material Market

The phase change material market is evolving rapidly as industries seek more efficient thermal management, energy savings, and improved comfort and safety. Phase change materials (PCMs) are increasingly integrated into building envelopes, cold-chain logistics, electronics cooling, textiles, and renewable energy systems to store and release heat in a controlled manner. Advances in encapsulation, bio-based chemistries, and smart controls are broadening performance ranges while lowering environmental impact. At the same time, regulatory pressure for greener buildings and low-carbon cooling solutions is accelerating demand. Together, these dynamics are reshaping the competitive landscape and creating new high-value application niches for PCMs worldwide.

Recent Developments in the Phase Change Material Market

The phase change material market is undergoing rapid transformation as industries prioritize energy efficiency, thermal comfort, and decarbonization. Growing adoption in construction, cold-chain logistics, textiles, and electronics cooling is driving innovation in both organic and inorganic PCMs, while regulations around building energy performance and sustainability targets are accelerating deployment. Manufacturers are focusing on higher energy density, improved cycling stability, and safer encapsulation methods to overcome historical reliability challenges. At the same time, collaboration between chemical companies, building system integrators, and HVAC players is expanding practical use cases and business models across global commercial, residential, and industrial applications.

Strategic Growth Opportunities in the Phase Change Material Market

The phase change material market is entering a strong growth trajectory as efficiency, decarbonization, and thermal resilience become core priorities across industries. Phase change materials (PCMs) offer latent heat storage that enables tighter temperature control, higher energy savings, and improved comfort or product stability. Rapid innovation in bio-based PCMs, encapsulation technologies, and system integration is widening their use from buildings and textiles to cold chain logistics and electronics. Regulatory pressure to cut emissions, combined with rising energy prices and electrification, is accelerating adoption. Five application areas stand out as the most attractive strategic growth opportunities for market participants.

Phase Change Material Market Drivers and Challenges

The global phase change material (PCM) market is shaped by a multifaceted set of technological, economic, and regulatory dynamics. Growing emphasis on energy efficiency, stricter building standards, and the need for temperature stability across diverse applications are creating solid momentum for PCM deployment. At the same time, issues such as high material costs, performance variability, and limited industry awareness constrain faster adoption. Technology advances in encapsulation, bio-based chemistries, and system integration are steadily improving the value proposition. Understanding the core drivers and challenges is essential for manufacturers, integrators, and end users seeking to capture long-term opportunities in this evolving market.

The factors responsible for driving the phase change material market include:

The challenges facing this phase change material market include:

The overall development of the global phase change material market reflects a tension between strong structural drivers and persistent implementation barriers. Rising energy costs, climate objectives, and growth in temperature-sensitive sectors are expanding the opportunity space for PCM-based thermal storage and regulation. However, cost, performance, and knowledge gaps continue to moderate the pace of adoption, especially in regions with less stringent energy regulations. Progress in materials science, encapsulation technologies, and application engineering is gradually mitigating these constraints. Stakeholders that invest in robust validation, cost optimization, and clear value communication are best positioned to benefit as the market matures.

List of Phase Change Material Market Companies

Companies in the market compete on the basis of product quality offered. Major players in this market focus on expanding their manufacturing facilities, R&D investments, infrastructural development, and leverage integration opportunities across the value chain. Through these strategies phase change material market companies cater increasing demand, ensure competitive effectiveness, develop innovative products & technologies, reduce production costs, and expand their customer base. Some of the phase change material market companies profiled in this report include-

Phase Change Material Market by Segment

The study includes a forecast for the global phase change material market by type, application, and region.

Country Wise Outlook for the Phase Change Material Market

The phase change material (PCM) market is evolving rapidly as countries seek advanced thermal management solutions for buildings, cold-chain logistics, electronics, and electric vehicles. PCMs, which store and release heat during phase transitions, are increasingly integrated into energy-efficient construction, temperature-controlled packaging, and battery systems. Recent developments reflect differing national priorities, from decarbonizing building stock to securing supply chains and fostering advanced materials innovation. The summaries below outline the latest trends and initiatives in the United States, China, Germany, India, and Japan, highlighting how each market is shaping demand, technology pathways, and commercialization of PCMs.

Features of the Phase Change Material Market

Article

Phase Change Material Market: Which Innovations Are Rewriting the Thermals Playbook?

Dallas, June 4, 2026 – The Phase Change Material (PCM) market is entering a decisive growth phase as energy efficiency, thermal management, and sustainability move from compliance topics to boardroom priorities. PCMs, which store and release heat during phase transitions such as solid-to-liquid, are shifting from niche thermal additives to strategic enablers across construction, electronics, cold chain logistics, mobility, and renewable energy systems. Momentum is being driven by stricter building codes, data center heat challenges, and the need to stabilize renewable energy, but the most disruptive impact is emerging where technology and thermal performance intersect.

Across the market, three to five major trends are reshaping business models: engineered bio-based and high-performance chemistries, integration of PCMs into smart systems, rapid adoption in electronics and batteries, and new business models in thermal services and circularity. These shifts are redefining which sectors capture value and which players risk being left behind as thermal performance becomes a differentiating feature instead of a hidden component cost.

Why Are Advanced PCM Chemistries Becoming a Strategic Differentiator?

The chemistry of PCMs is moving beyond basic paraffins and salt hydrates toward highly engineered formulations aimed at specific temperature windows, lifespan, and safety requirements. Stakeholders are increasingly demanding materials that not only deliver precise thermal performance but also align with ESG commitments and regulatory expectations. This shift is opening new product categories and reshuffling the competitive landscape among materials suppliers and specialty chemical companies.

Buildings, refrigerated transport, and renewable energy storage markets are expected to see significant impact from these chemistry advances. More stable and safer PCMs unlock integration into structural building elements and façade systems, while higher-temperature materials support industrial demand response and heat storage. As chemistries become more customizable, suppliers that can co-develop formulations with OEMs and integrators will capture disproportionate value.

How Is Smart Integration of PCMs Transforming Buildings and Energy Systems?

Standalone PCM products are giving way to integrated thermal systems that combine materials, sensors, controls, and digital optimization. In the built environment, PCMs are increasingly embedded in wallboards, ceiling tiles, flooring systems, and HVAC components to blunt peak loads and smooth indoor temperatures. When combined with intelligent controls, these materials enable time-shifting of cooling and heating, turning passive structures into active thermal assets.

These smart integrations are expected to disrupt traditional cooling capacity planning and energy procurement models. Utilities and energy service companies are beginning to view PCM-equipped buildings and facilities as flexible thermal batteries that can be monetized in demand response and ancillary services markets. This creates opportunities for new partnerships between materials firms, automation vendors, and energy retailers built around performance guarantees rather than simple product sales.

Where Will the Technology Industry Feel the Strongest Impact of PCM Innovation?

The technology industry is emerging as one of the most dynamic demand centers for advanced PCMs, driven by escalating heat densities, miniaturization, and the electrification of mobility. Data centers, high-performance computing, consumer electronics, and electric vehicles are all confronting the limits of conventional air cooling and simple heat sinks. In this environment, PCMs are moving from experimental concepts to standard design options in product roadmaps.

These use cases are poised to disrupt traditional thermal design workflows and supplier hierarchies in the electronics value chain. As device makers embed PCMs deeper into their architectures, Tier 1 and Tier 2 suppliers with advanced materials expertise and strong co-design capabilities will gain leverage. Thermal performance may become a key differentiator not only for flagship devices but also for cloud services, charging networks, and mobility platforms.

Which Markets Stand to Gain Most from PCM-Driven Disruption?

While PCMs touch many sectors, several markets are positioned for outsized impact as innovations scale and costs decline. These markets combine large thermal footprints, clear pain points, and regulatory or customer pressures that reward smarter heat management.

Across these markets, the disruption is not merely technical. Business models are shifting toward performance-based contracts, thermal-as-a-service, and integrated energy solutions, where PCMs become hidden but critical enablers of new revenue streams and cost structures.

What Are the Main Challenges Holding Back Wider PCM Adoption?

Despite rising interest and a richer innovation pipeline, the PCM market continues to face structural and operational barriers that slow scale-up. Many of these challenges are not purely material-science issues but relate to integration complexity, standards, and fragmented value chains.

Overcoming these barriers will require coordinated efforts among materials suppliers, standards bodies, regulators, and system integrators. Demonstration projects, open data on long-term performance, and clear labeling will play pivotal roles in building confidence and accelerating broader deployment.

Where Do the Biggest Opportunities Emerge for Innovators and Investors?

The evolving PCM landscape offers attractive openings for both established corporates and new entrants willing to build capabilities across materials, systems engineering, and digital services. The most compelling opportunities lie where PCMs intersect with decarbonization, electrification, and digitalization agendas.

What Recent Developments Signal the Next Phase of Market Maturity?

Recent activity across the PCM value chain illustrates how the market is moving from experimental pilots to more mature, repeatable deployments. While specific corporate announcements vary by region and segment, several patterns are emerging that point to the next stage of competition and consolidation.

These developments suggest that the phase change material market is entering a scale-up phase characterized by sector-specific solutions, performance data, and closer alignment with policy and sustainability frameworks. For executives and investors, the message is clear: PCMs are transitioning from a specialized thermal niche to a strategic lever in energy, technology, and infrastructure transformation. Those who move early to understand, integrate, and commercialize these materials within broader systems will be better positioned to capture emerging value and shape the next wave of thermal innovation.

Top 5 Companies

1. BASF

BASF is one of the largest global chemical companies and a leading supplier of advanced materials, including phase change materials (PCMs) used for thermal energy storage and temperature control applications. Headquartered in Ludwigshafen, Germany, and established in 1865, BASF employs well over 100,000 people worldwide and operates production sites and R&D centers across Europe, North America, Asia Pacific, South America, and the Middle East. In the phase change material market, BASF’s portfolio includes organic, inorganic, and bio-based PCMs tailored for building envelopes, interior plasters, wallboards, ceiling systems, refrigerated transport, cold-chain packaging, and temperature-controlled logistics. These materials are integrated into construction products to reduce heating and cooling loads, enhance energy efficiency, and support net-zero building designs. BASF has expanded its geographic reach for PCM-related solutions by collaborating with building materials manufacturers and insulation system providers in Europe and North America and by promoting PCM-enhanced solutions in rapidly urbanizing regions in Asia. The company regularly enters technology partnerships and joint development agreements with construction firms, HVAC manufacturers, and packaging specialists to co-develop PCM-integrated systems. While BASF’s mergers and acquisitions are broad-based across chemicals and materials, its acquisitions of specialty chemicals businesses and building materials portfolios have reinforced its capabilities in energy-efficient construction and thermal management, indirectly strengthening its PCM business and global offering.

2. Honeywell

Honeywell is a diversified technology and manufacturing company with strong positions in building technologies, performance materials, and aerospace, and it participates in the phase change material market through its advanced materials and building solutions businesses. Headquartered in Charlotte, North Carolina, and founded in 1906, Honeywell employs more than 90,000 people and serves customers in over 100 countries. Within the PCM domain, Honeywell develops and supplies specialty chemicals, encapsulated PCMs, and thermal management solutions used in building envelopes, energy-efficient roofing, chilled ceilings, cold-chain logistics, electronics cooling, and battery thermal management. Its PCMs are designed to smooth temperature peaks, store surplus energy, and improve overall system efficiency in both residential and commercial buildings as well as in industrial applications. The company has a broad geographic footprint across North America, Europe, the Middle East, Asia Pacific, and Latin America, with local engineering support and integration capabilities that enable PCM deployment in region-specific building codes and climatic conditions. Honeywell has expanded its presence in energy-efficient buildings and advanced materials through investments and partnerships focused on smart buildings and sustainable infrastructure, where PCMs are often integrated with controls and sensors. While Honeywell’s major mergers and acquisitions span automation, software, and specialty materials, the acquisition and integration of performance materials and building technologies businesses have allowed it to bundle PCMs with insulation, HVAC controls, and building management systems, strengthening its position in the global phase change material market.

3. Dow

Dow is a leading global materials science company that offers a wide portfolio of specialty polymers, chemicals, and advanced materials, including solutions relevant to the phase change material market. Headquartered in Midland, Michigan, and founded in 1897, Dow employs tens of thousands of people and operates manufacturing and R&D facilities across North and South America, Europe, the Middle East, Africa, and Asia Pacific. In the PCM space, Dow focuses on enabling technologies such as encapsulation polymers, binders, and formulation components that are used in microencapsulated PCMs for building materials, textiles, and thermal packaging. Dow’s materials are widely used in wallboards, plasters, roofing membranes, and insulation products that incorporate PCMs for improved thermal comfort and reduced energy consumption. The company also supports PCMs for cold-chain and temperature-sensitive logistics through high-performance foams and encapsulation resins. Dow has extended its geographic presence by partnering with regional construction material producers, packaging companies, and appliance manufacturers to integrate PCM-capable materials into local product lines. Its global innovation centers collaborate closely with OEMs to tailor PCM-related solutions to climatic and regulatory requirements in key markets such as Europe, China, and North America. Dow’s broader M&A activity, including portfolio rationalization and targeted acquisitions in performance materials, has bolstered its capabilities in advanced building and packaging solutions. These moves support the development and commercialization of PCM-containing systems, helping customers design more energy-efficient buildings, appliances, and logistic chains that benefit from controlled thermal management and improved sustainability.

4. Phase Change Energy Solutions

Phase Change Energy Solutions is a specialized company dedicated to the development and commercialization of phase change materials and PCM-enabled products for energy efficiency and thermal management. Headquartered in Asheboro, North Carolina, and established in 2004, the company focuses on engineered PCMs derived from bio-based and hybrid formulations designed for predictable melting and freezing temperatures. While exact employee numbers are not publicly detailed, Phase Change Energy Solutions operates with a focused team serving customers in North America and expanding into Europe, the Middle East, and Asia through distributors and partners. Its product portfolio includes PCM-enhanced building panels, ceiling tiles, insulation systems, cold-chain and refrigerated packaging solutions, data center thermal management products, and textile applications. Branded PCM solutions are integrated into commercial and residential buildings to reduce peak loads and improve occupant comfort, and into logistics systems to maintain temperature for food, pharmaceuticals, and other temperature-sensitive goods. The company has expanded its geographic reach by forming alliances with building system integrators, HVAC firms, and packaging companies in Europe and the Middle East and by participating in demonstration projects and pilot installations in diverse climates. Phase Change Energy Solutions has also entered strategic collaborations and licensing agreements with global construction and technology firms to embed its PCMs into established product lines. While it has not announced large headline mergers or acquisitions, it has pursued technology partnerships and smaller asset or IP deals that strengthen its PCM chemistry, encapsulation know-how, and manufacturing capabilities, reinforcing its position as a dedicated player in the global phase change material market.

5. Rubitherm

Rubitherm is a Germany-based specialist in phase change materials and PCM systems, recognized for its broad catalog of standard and customized PCMs serving a wide range of thermal energy storage applications. Founded in 1993 and headquartered in Berlin, Rubitherm focuses almost exclusively on PCMs, offering a portfolio that includes organic, inorganic, and eutectic formulations as well as macro- and micro-encapsulated products. The company serves customers across Europe and internationally, with distributors and partners extending its reach into Asia, North America, and other regions. While specific employee counts are not widely disclosed, Rubitherm operates as a focused technology company with in-house development and production capabilities. Its PCM products are used in building and construction, refrigeration and cold-chain logistics, solar thermal storage, waste-heat recovery, HVAC systems, electronics cooling, and temperature-sensitive packaging. Rubitherm supplies PCMs in containers, plates, spheres, and other formats tailored for integration into building components, storage tanks, and transport systems. Over recent years, the company has expanded its geographic presence by enhancing export activities and partnering with system integrators and OEMs in building technology, renewable energy, and mobility sectors that incorporate PCMs into their solutions. Rubitherm concentrates on organic growth, technical collaborations, and joint development agreements rather than large-scale mergers and acquisitions. Its strategic focus is on improving PCM reliability, cycling stability, and environmental performance, thereby reinforcing its niche leadership in the global phase change material market and supporting customers who require precise and durable thermal management solutions.

Table of Contents

List of Figures

List of Tables

Methodology

Lucintel has been in the business of market research and management consulting since 2000 and has published over 1000 market intelligence reports in various markets / applications and served over 1,000 clients worldwide. This study is a culmination of four months of full-time effort performed by Lucintel's analyst team. The analysts used the following sources for the creation and completion of this valuable report:

- In-depth interviews of the major players in this market

- Detailed secondary research from competitors' financial statements and published data

- Extensive searches of published works, market, and database information pertaining to industry news, company press releases, and customer intentions

- A compilation of the experiences, judgments, and insights of Lucintel's professionals, who have analyzed and tracked this market over the years.

Extensive research and interviews are conducted across the supply chain of this market to estimate market share, market size, trends, drivers, challenges, and forecasts. Below is a brief summary of the primary interviews that were conducted by job function for this report.

Thus, Lucintel compiles vast amounts of data from numerous sources, validates the integrity of that data, and performs a comprehensive analysis. Lucintel then organizes the data, its findings, and insights into a concise report designed to support the strategic decision-making process. The figure below is a graphical representation of Lucintel's research process.

Buy Now

Choose a license that fits your team. Instant PDF delivery.

Prices exclude taxes. Instant delivery. Custom licensing available on request.

Frequently Asked Questions

What is the Phase Change Material Market size?

What is the growth forecast for Phase Change Material Market?

What are the major drivers influencing the growth of the Phase Change Material Market?

What are the major segments for Phase Change Material Market?

Who are the key Phase Change Material Market companies?

Which Phase Change Material Market segment will be the largest in future?

In Phase Change Material Market, which region is expected to be the largest in next 9 years?

Do we receive customization in this report?

Key Questions

- • What are some of the most promising, high-growth opportunities for the Phase Change Material Market by Type (Organic, Inorganic, and Others), Application (Building & Construction, HVAC, Cold Chain & Packaging, Electronics, Textiles, and Others), and region (North America, Europe, Asia Pacific, and the Rest of the World)?

- • Which segments will grow at a faster pace and why?

- • Which region will grow at a faster pace and why?

- • What are the key factors affecting market dynamics? What are the key challenges and business risks in this market?

- • What are the business risks and competitive threats in this market?

- • What are the emerging trends in this market and the reasons behind them?

- • What are some of the changing demands of customers in the market?

- • What are the new developments in the market? Which companies are leading these developments?

- • Who are the major players in this market? What strategic initiatives are key players pursuing for business growth?

- • What are some of the competing products in this market and how big of a threat do they pose for loss of market share by material or product substitution?

- • What M&A activity has occurred in the last 9 years, and what has its impact been on the industry?