Report Feature

Laser Direct Imaging (LDI) Equipment Market Trends and Forecast

The technologies in the laser direct imaging (LDI) equipment market have undergone significant changes in recent years, with a shift from 350-375nm light sources to 375-410nm light sources. This transition has been driven by the need for higher precision, better resolution, and improved production efficiency. Achieving finer feature definition and more efficient imaging is possible with the 375-410nm light source, which is ideal for advanced applications such as HDI PCBs and IC substrates. These more recent light sources offer higher power efficiency and faster processing speeds, which are crucial in highly miniaturized and performance-demanding fields such as electronics. Equipment Market")

Emerging Trends in the Laser Direct Imaging (LDI) Equipment Market

The laser direct imaging (LDI) equipment market is experiencing several transformative trends driven by technological improvements and changing industry demands. This section highlights five key trends shaping the future of this market:• Transition to Higher Wavelength Light Sources (375-410nm): The move towards 375-410nm light sources brings higher resolution and power efficiency, which helps manufacturers make smaller, more complex PCBs and IC substrates. This is essential for industries requiring high-density interconnections and precision in circuit designs.

• Increased Adoption in HDI PCB Production: High-density interconnect (HDI) PCBs require precise, high-resolution imaging for efficient multi-layered circuit designs. Laser direct imaging technology’s ability to provide fine resolution is driving its increased adoption in HDI PCB production, offering cost-effective and scalable solutions for complex electronic devices.

• Integration of Automation and AI in laser direct imaging Equipment: The integration of automation and AI-based technologies in laser direct imaging equipment makes the imaging process more accurate and efficient. AI-powered inspection systems maintain optimal alignment and quality while reducing human error, which, in turn, increases production throughput.

• Multilayer PCBs in Consumer Electronics: As consumer electronics, especially smartphones, wearable devices, and laptops, move towards higher functionality in smaller form factors, the demand for multilayer PCBs is on the rise. laser direct imaging technology is well-positioned to meet this market need, given its ability to handle intricate, multi-layer designs.

• Eco-Friendly and Energy-Efficient Equipment Shift: Environmental concerns and energy efficiency have become primary focuses for manufacturers today. New developments in laser direct imaging equipment emphasize lower energy consumption and reduced environmental harm, assisting companies in meeting sustainability goals without compromising high-performance production standards. Trends in the laser direct imaging (LDI) equipment market are reshaping the industry by enabling greater precision, supporting complex and high-density designs, and improving overall production efficiency. These advances are positioning laser direct imaging technology at the forefront of critical enablers for the future of electronics manufacturing.

Equipment Heat Map")

Laser Direct Imaging (LDI) Equipment Market : Industry Potential, Technological Development, and Compliance Considerations

Laser direct imaging (LDI) technology is used in the production of printed circuit boards (PCBs), flat-panel displays, and photomasks. Laser direct imaging equipment utilizes laser beams to directly image circuit patterns onto substrates with high precision, replacing traditional photolithography methods. This technology offers significant advantages in terms of resolution, accuracy, and the ability to handle fine features in electronic devices, making it critical for the evolving electronics industry, including telecommunications, automotive, and consumer electronics.• Technology Potential: The potential of laser direct imaging technology lies in its ability to enhance the speed, resolution, and cost-effectiveness of PCB manufacturing. As electronic devices become smaller and more complex, the demand for fine-line imaging grows. Laser direct imaging systems can achieve finer patterning with higher accuracy, allowing for faster production cycles and better overall quality control. Additionally, the elimination of photomasks reduces material costs and setup times, providing both economic and operational advantages in mass production.

• Degree of Disruption: Laser direct imaging technology is moderately disruptive to PCB manufacturing as it enables manufacturers to keep pace with the miniaturization trend in electronics. It has the potential to transform circuit board production, particularly in advanced technologies like 5G, AI, and IoT, where high-density, complex PCB designs are essential.

• Technology Maturity: Laser direct imaging technology is relatively mature, with established solutions widely used in PCB production. However, the precision of lasers, imaging resolution, and process speed are still being improved due to ongoing developments.

• Regulatory Compliance: Laser direct imaging equipment, particularly in light of environmental changes, is subject to regulations under RoHS (Restriction of Hazardous Substances) and CE certification. They must be strictly environmentally friendly for use. Manufacturers must meet all safety regulations regarding the equipment used in manufacturing to ensure the safety of the final products.

Recent Technological development in Laser Direct Imaging (LDI) Equipment Market by Key Players

Leading laser direct imaging equipment companies must continually innovate to stay ahead of competition and meet the rising demand from the electronics industry. Here are a few recent developments from leading companies like Orbotech, HANS Laser Technology, Fujifilm, and others:• Orbotech: Orbotech, an laser direct imaging equipment provider, has developed advanced imaging systems with 375-410nm light sources. These offer more accuracy and throughput in PCB and IC substrate production. Their innovations allow manufacturers to meet the demands of HDI and multilayer PCB designs with increased efficiency.

• HANS Laser Technology: HANS Laser Technology has launched next-generation laser direct imaging systems that combine high-resolution light sources with enhanced software solutions. These systems focus on automating the imaging process to reduce human error and improve overall production efficiency, especially for HDI PCBs and multilayer circuit boards.

• ORC Manufacturing: ORC has been actively working to enhance the speed and accuracy of their laser direct imaging equipment by using high-wavelength light sources and automated systems for better alignment and imaging. Their solutions are designed to address the increasing need for miniaturized PCBs in consumer electronics and automotive applications.

• Fujifilm: Fujifilm has expanded its laser direct imaging product portfolio with advanced systems designed for low energy consumption and environmentally friendly products. The systems are optimized for high-resolution imaging and are increasingly used in the production of HDI PCBs and IC substrates.

• Hitachi: Hitachi unveiled new laser direct imaging equipment infused with AI. The system automatically inspects and performs real-time quality control checks. As a result, each board is strictly qualified, providing a valuable solution for high-demand markets such as telecommunications, automotive, and consumer electronics.

• CAIZ OPTRONICS CORP: CAIZ OPTRONICS has focused on making their laser direct imaging equipment more efficient and versatile by allowing their systems to accommodate complex multilayer PCB designs. Their products are well-suited for high-performance electronics applications, such as aerospace and defense.

• SCREEN Holdings: SCREEN Holdings has significantly improved its laser imaging systems by emphasizing automation, precision, and energy efficiency. These systems are commonly used in the production of multilayer PCBs and IC substrates, delivering fast production speeds with minimal waste. These developments demonstrate how industry leaders are innovating to meet demands for precision, efficiency, and sustainability in the marketplace. They are doing so through technological advancements and preparing to capture a share of the growing market for HDI PCBs, multilayer PCBs, and IC substrates.

Laser Direct Imaging (LDI) Equipment Market Driver and Challenges

The laser direct imaging equipment market is driven by several factors and faces numerous challenges that affect its growth. Here are some of the key drivers and challenges influencing the future of the LDI market: The factors responsible for driving the laser direct imaging (LDI) equipment market include:• Increased Demand for HDI and Multilayer PCBs: As electronics become miniaturized and more complex, there is increasing demand for HDI and multilayer PCBs. LDI technology is in high demand because it ensures high precision and can accommodate complex designs.

• Advances in Light Source Technology: The transition to higher wavelength light sources (375-410nm) enables LDI equipment to produce finer features with more accuracy, improving production capabilities and satisfying the demand for small, complex circuit designs.

• Increased Automation in PCB Manufacturing: The integration of automation into LDI systems leads to higher efficiency and lower error rates in PCB production. Automated systems streamline manufacturing, enabling faster production times.

• Demand for Energy-Efficient and Sustainable Manufacturing: The demand for more sustainable and energy-efficient manufacturing processes is driving the development of LDI equipment that consumes less energy and produces fewer emissions. This is particularly relevant for industries striving to meet environmental standards and reduce operational costs. Challenges in the laser direct imaging (LDI) equipment market include:

• High Initial Investment: Installing LDI systems can be costly, particularly for small and medium-sized manufacturers. The high cost of entry may deter adoption, especially in price-sensitive markets.

• Complexity of Integrating New Technologies: Integrating advanced LDI systems into existing manufacturing lines can be a complex and costly process. Manufacturers need to train personnel and ensure compatibility with existing equipment, which can delay adoption and increase operational costs.

• Technological Obsolescence: With rapid advancements in technology, LDI systems can become obsolete quickly, forcing manufacturers to constantly update their equipment to remain competitive. This need for continuous upgrades and innovations can lead to higher costs and faster depreciation. The laser direct imaging equipment equipment market is driven by the increasing demand for high-precision PCBs and energy-efficient manufacturing solutions. However, challenges such as high initial investments, integration complexities, and technological obsolescence must be addressed to sustain growth. As companies adapt to these challenges, LDI technology is poised to remain a key enabler of innovation in the electronics manufacturing industry.

List of Laser Direct Imaging (LDI) Equipment Companies

Companies in the market compete based on product quality offered. Major players in this market focus on expanding their manufacturing facilities, R&D investments, infrastructural development, and leverage integration opportunities across the value chain. With these strategies laser direct imaging (LDI) equipment companies cater to increasing demand, ensure competitive effectiveness, develop innovative products & technologies, reduce production costs, and expand their customer base. Some of the laser direct imaging (LDI) equipment companies profiled in this report include.• Orbotech

• HANS Laser Technology

• ORC Manufacturing

• Fujifilm

• Hitachi

• CAIZ OPTRONICS CORP

Laser Direct Imaging (LDI) Equipment Market by Technology

• Technology Readiness of Light Sources: 350-375nm and 375-410nm for the Laser Direct Imaging (LDI) Equipment Market: The 350-375nm light source technology is mature and ready for high-precision use in sectors such as semiconductor manufacturing, PCB fabrication, and advanced optics, thanks to its ability to achieve finer patterns with exceptional accuracy. This technology has reached a high level of readiness and is proven to create the fine geometries required by modern electronics. The 375-410nm light source is slightly less mature in terms of resolution but is widely used in mid-range applications, balancing cost and performance for industries that do not require the highest precision. Competitive pressures are intense, with companies developing cutting-edge 350-375nm technology to maintain an advantage in high-resolution markets, while 375-410nm systems continue to dominate in more cost-sensitive sectors. Regulatory compliance ensures that safety and performance standards are met, particularly for the safe use of UV lasers and adherence to environmental regulations regarding energy consumption and emissions. As demand for more compact, precise, and energy-efficient solutions grows, both light sources will evolve to meet the needs of the rapidly changing market.

• Competitive Intensity and Regulatory Compliance of Light Source: 350-375nm and 375-410nm for the Laser Direct Imaging (LDI) Equipment Market: The competitive intensity in the LDI equipment market is increasing, with players competing to provide more efficient light sources with higher resolution. The 350-375nm light source technology is the new favorite for high-resolution imaging applications in the semiconductor and PCB industries, giving companies using this wavelength a competitive edge. However, 375-410nm light sources remain strong in markets focused on cost, energy efficiency, and speed. Regulatory compliance is critical for both technologies, particularly concerning safety standards for UV light emissions and their effects on workers and the environment. LDI systems must comply with international standards regarding environmental sustainability, energy efficiency, and worker safety, especially in controlling UV lasers in commercial applications. In the future, the adoption of these light sources across industries will be determined by adherence to these regulations as the technology continues to evolve.

• Potential Disruption by the Light Source: 350-375nm and 375-410nm in the Laser Direct Imaging (LDI) Equipment Market: The laser direct imaging (LDI) equipment market is being disrupted by the shift in light source technologies. Light sources operating in the 350-375nm range are becoming increasingly popular due to their better resolution and finer pattern capabilities. These are recommended for high-precision applications in electronics, PCB manufacturing, and microelectronics. Meanwhile, light sources in the 375-410nm range, with slightly lower resolution but better energy efficiency, are becoming popular for broader industrial applications where cost-effectiveness and speed are prioritized. The disruption arises from the increased adoption of shorter-wavelength (350-375nm) light sources that enable more precise imaging, pushing older and less efficient 375-410nm sources out of high-end markets. This shift is likely to change the landscape of LDI equipment as manufacturers adopt newer, higher-performance systems to meet the growing demand for miniaturization and high-resolution imaging.

Laser Direct Imaging (LDI) Equipment Market Trend and Forecast by Technology [Value from 2019 to 2031]:

• Light Source: 350-375nm

• Light Source: 375-410 nm

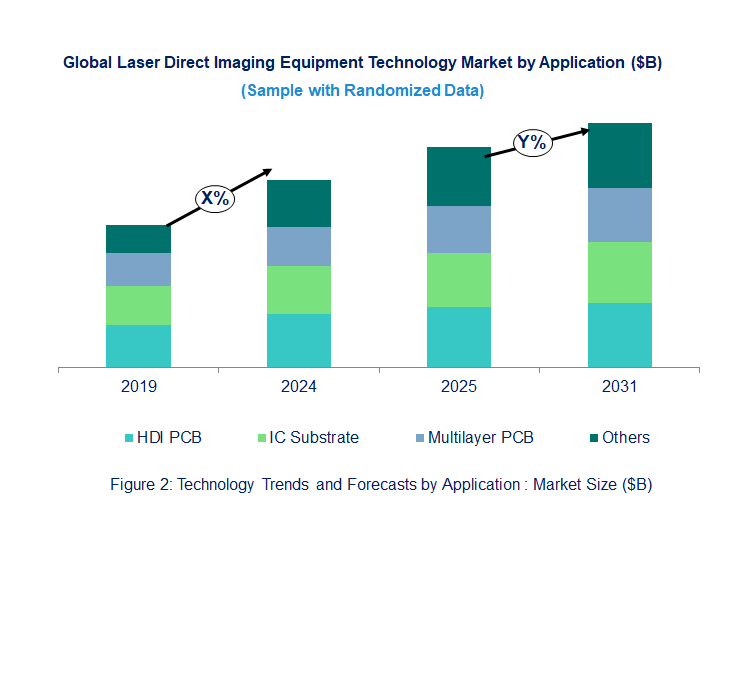

Laser Direct Imaging (LDI) Equipment Market Trend and Forecast by Application [Value from 2019 to 2031]:

• HDI PCB

• IC Substrate

• Multilayer PCB

• Others

Laser Direct Imaging (LDI) Equipment Market by Region [Value from 2019 to 2031]:

• North America

• Europe

• Asia Pacific

• The Rest of the World

• Latest Developments and Innovations in the Laser Direct Imaging (LDI) Equipment Technologies

• Companies / Ecosystems

• Strategic Opportunities by Technology Type

Features of the Global Laser Direct Imaging (LDI) Equipment Market

Market Size Estimates: Laser direct imaging (LDI) equipment market size estimation in terms of ($B). Trend and Forecast Analysis: Market trends (2019 to 2024) and forecast (2025 to 2031) by various segments and regions. Segmentation Analysis: Technology trends in the global laser direct imaging (LDI) equipment market size by various segments, such as application and technology in terms of value and volume shipments. Regional Analysis: Technology trends in the global laser direct imaging (LDI) equipment market breakdown by North America, Europe, Asia Pacific, and the Rest of the World. Growth Opportunities: Analysis of growth opportunities in different applications, technologies, and regions for technology trends in the global laser direct imaging (LDI) equipment market. Strategic Analysis: This includes M&A, new product development, and competitive landscape for technology trends in the global laser direct imaging (LDI) equipment market. Analysis of competitive intensity of the industry based on Porter’s Five Forces model.Table of Contents

Methodology

- In-depth interviews of the major players in this market

- Detailed secondary research from competitors’ financial statements and published data

- Extensive searches of published works, market, and database information pertaining to industry news, company press releases, and customer intentions

- A compilation of the experiences, judgments, and insights of Lucintel’s professionals, who have analyzed and tracked this market over the years.

Buy Now

Choose a license that fits your team. Instant PDF delivery.

Prices exclude taxes. Instant delivery. Custom licensing available on request.

Key Questions

- • What are some of the most promising potential, high-growth opportunities for the technology trends in the global laser direct imaging (ldi) equipment market by technology (light source: 350-375nm and light source: 375-410 nm), application (hdi pcb, ic substrate, multilayer pcb, and others), and region (North America, Europe, Asia Pacific, and the Rest of the World)?

- • Which technology segments will grow at a faster pace and why?

- • Which regions will grow at a faster pace and why?

- • What are the key factors affecting dynamics of different technology? What are the drivers and challenges of these technologies in the global laser direct imaging (LDI) equipment market?

- • What are the business risks and threats to the technology trends in the global laser direct imaging (LDI) equipment market?

- • What are the emerging trends in these technologies in the global laser direct imaging (LDI) equipment market and the reasons behind them?

- • Which technologies have potential of disruption in this market?

- • What are the new developments in the technology trends in the global laser direct imaging (LDI) equipment market? Which companies are leading these developments?

- • Who are the major players in technology trends in the global laser direct imaging (LDI) equipment market? What strategic initiatives are being implemented by key players for business growth?

- • What are strategic growth opportunities in this laser direct imaging (LDI) equipment technology space?

- • What M & A activities did take place in the last five years in technology trends in the global laser direct imaging (LDI) equipment market?